.png)

Decoding the Customs Act 1962: A Comprehensive Guide

Optimize your business: use unlimited savings with Pazago fulfilled now!

Get Started ->A shipment is packed, the container gated in, and the vessel cut-off is met. Yet the cargo does not move. Customs raises a query on classification. The shipping bill is held. Your buyer starts asking for revised delivery dates. What looked like a routine dispatch becomes a commercial risk.

This is where the Customs Act, 1962, directly affects Indian exporters. It is not just a legal framework sitting in the background. It governs how your goods are assessed, cleared, inspected, valued, and even penalised. In 2026, with faceless assessments, data-driven risk systems, and tighter enforcement, the Act continues to shape how predictably you can move goods across borders.

This guide explores the structure of the Customs Act, 1962, its key provisions, types of duties, compliance responsibilities, penalties, recent amendments, and how it influences your export operations.

Key Takeaways:

- The Customs Act, 1962, governs assessment, clearance, valuation, inspection, and enforcement for export and import shipments at the Indian borders.

- Duty assessment rules, prohibited and restricted goods provisions, documentation accuracy, and officer powers directly impact shipment release timelines, port detention risk, and compliance exposure.

- BCD, IGST, export duty, anti-dumping duty, safeguard duty, Social Welfare Surcharge, and scheme-linked exemptions influence input cost, pricing strategy, and refund cycles.

- Defined exporter obligations, officer authority, mandatory licences such as IEC and LUT, penalty provisions, and recent amendments like voluntary revision and extended advance ruling validity shape day-to-day compliance decisions.

- Clearance delays, RMS-triggered inspections, refund bottlenecks, detention charges, contractual risks, and documentation mismatches affect working capital, delivery timelines, and export competitiveness.

What is the Customs Act, 1962

At its core, the Customs Act, 1962, is the principal Indian legislation that governs how goods are assessed, cleared, taxed, and regulated at India’s borders, whether they are heading out as exports or coming in as imports.

For an exporter, this Act matters because it defines:

- How customs duties apply (even if export duty is zero on most shipments)

- What documentation must be submitted

- What risks do you face if the paperwork is wrong or incomplete

- How customs officers can act on your goods

The Act’s provisions shape the clearance time, compliance costs, and risk of seizure or penalties that directly affect your ability to meet buyer timelines and maintain margins if classification or valuation is disputed.

Purpose and Objectives

The Customs Act was enacted to regulate the cross-border movement of goods and safeguard government revenue. But its objectives go beyond revenue collection and directly affect how your shipments are screened and assessed.

It aims to:

- Prevent smuggling and illegal trade

- Ensure proper classification and valuation

- Facilitate legitimate trade while maintaining enforcement controls

For exporters, this means every shipment is subject to scrutiny not only for tax compliance but also for regulatory and security reasons. Even genuine errors in HS classification, product description, or declared value can trigger examination or reassessment.

With that foundation, let’s examine the major provisions exporters encounter in day-to-day operations.

Also Read: Customs Charges in India: Types, Calculation & When They Apply

Major Provisions within the Customs Act 1962

The Customs Act contains numerous sections, but exporters regularly interact with specific operational provisions that affect shipping bills, valuation, assessment, confiscation, and penalties.

Below are the provisions that most directly affect Indian exporters.

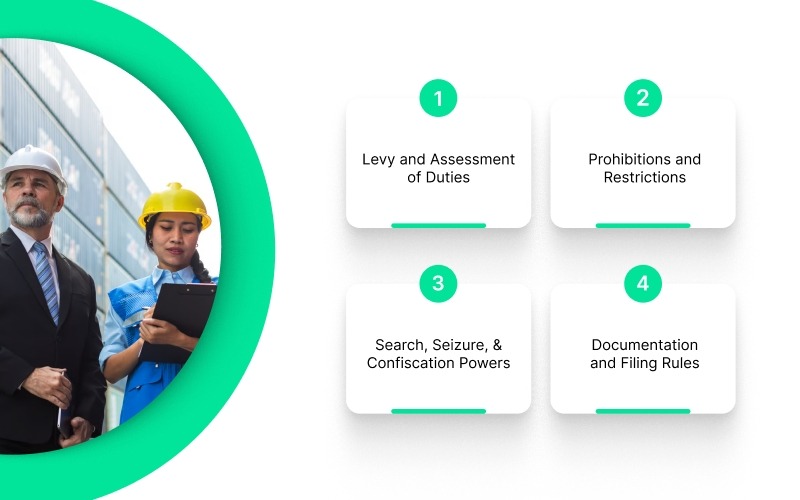

1. Levy and Assessment of Duties

Under Sections 12 and related provisions, customs duty is normally levied on imported goods, but also applies to exports for specific categories or rebates where applicable.

For exporters:

- Duty liability is often zero for finished export goods, but other levies like IGST and cesses may be involved, and mistakes here lead to denied refunds or penalty notices.

- Goods that fall under restricted or prohibited categories still attract strict scrutiny and confiscation risk if improperly declared.

2. Prohibitions and Restrictions

The Act allows the government to prohibit or restrict the export of certain items, often aligned with foreign trade policy or safety standards.

If you export:

- Restricted items without an appropriate licence or permit (e.g., strategic goods, chemicals), goods can be confiscated, and fines imposed.

- Misclassification of a good’s HS code can also trigger a restriction — leading to greater duty liabilities or enforcement scrutiny.

3. Search, Seizure, and Confiscation Powers

Customs officers have statutory authority to inspect, detain, and even confiscate goods if they suspect violations.

For exporters, this means:

- Incorrect documentation, under-valuation, or misclassification can result in your shipment being held or seized.

- To avoid these outcomes, exporters must proactively verify HS codes, shipping bills, and licence requirements.

4. Documentation and Filing Rules

The Act and related rules require:

- Accurate shipping bills

- Correct GST documentation

- IEC, LUT, and other trade certificates

Mistakes in these filings are the most frequent causes of customs delays. Ensuring precise documentation reduces assessment errors and prevents costly hold-ups.

These provisions make it essential to understand the duty structure that interacts with them.

Types of Customs Duties in India

Although exports from India are generally zero-rated, the Customs Act and related tariff laws define multiple types of duties that influence exporter pricing and compliance decisions.

Understanding duty structure is essential for pricing, cost forecasting, and incentive calculation.

1. Basic Customs Duty (BCD)

Basic Customs Duty primarily applies to imported goods. However, many exporters import raw materials, components, or capital goods for manufacturing export products.

If you are importing inputs under schemes like Advance Authorisation or EPCG, BCD may be exempted, subject to export obligations. Failure to fulfil those obligations can trigger full duty recovery with interest.

What exporters should monitor:

- Conditions attached to duty exemption schemes

- Export obligation timelines

- Proper documentation linking imports to exports

- Record maintenance for audit verification

A common mistake is treating an exemption as permanent relief. In reality, it is conditional and performance-linked.

2. Integrated Goods and Services Tax (IGST)

Exports from India are zero-rated under GST. Exporters have two options:

- Export under LUT (without paying IGST)

- Pay IGST on export and claim a refund later

Both routes require accurate shipping bill filing and GST return matching. Even minor mismatches between invoice details and shipping bill entries can delay refunds.

Why this matters commercially:

- Delayed IGST refunds affect working capital

- Incorrect filings increase compliance queries

- Repeated mismatches may increase scrutiny

Exporters often focus only on dispatch timelines but overlook refund processing timelines, which directly impact liquidity.

3. Export Duty

Certain goods attract export duty based on government policy. This typically applies to specific minerals, metals, or agricultural commodities during periods of domestic supply control.

Export duty directly increases your FOB cost. If not factored correctly while negotiating with overseas buyers, it reduces the margin.

Before finalising contracts, exporters should:

- Verify current export duty notifications

- Check if duty rates are ad hoc or time-bound

- Assess the impact on long-term supply agreements

Export duty changes can occur through notifications. Pricing contracts without monitoring updates creates avoidable financial exposure.

4. Anti-Dumping Duty

Anti-dumping duty is imposed on certain imported goods to protect domestic industries. While this applies to imports, exporters importing affected raw materials experience higher input costs.

This indirect cost pressure influences export competitiveness.

Operational implications include:

- Increased production cost

- Need for alternative sourcing

- Pricing renegotiation with buyers

Exporters often calculate pricing based on historical raw material costs. If anti-dumping duties are imposed mid-cycle, margins can shrink unexpectedly.

5. Safeguard Duty

Safeguard duty is applied temporarily to protect domestic industries from sudden import surges. Like anti-dumping duty, it mainly affects importers, but exporters dependent on imported inputs must factor in cost fluctuation.

Because safeguard duties are usually time-bound, exporters should track notification validity carefully.

Key considerations:

- Duration of the safeguard measure

- Whether exemptions apply to export-oriented units

- Contractual flexibility with buyers

Ignoring time-bound duty changes may lead to either overpricing or underpricing in international markets.

6. Social Welfare Surcharge (SWS)

Social Welfare Surcharge is calculated as a percentage of Basic Customs Duty on imports. Exporters importing inputs under schemes should verify whether the SWS exemption applies.

Even when BCD is exempt under a scheme, surcharge applicability may vary depending on notification conditions.

Why this is important:

- SWS can increase the effective import cost

- Incorrect calculation may lead to reassessment

- Scheme-based exemptions must be reviewed carefully

Many exporters overlook surcharge components while calculating landed input cost, which affects final export pricing.

7. Additional Duties Under Special Schemes

Certain exports may interact with:

- Countervailing measures

- Special additional duties

- Cess or sector-specific levies

These depend on product category and trade policy changes.

Instead of assuming uniform duty treatment, exporters should regularly review notifications relevant to their HS classification. Duty structure is dynamic and policy-driven.

Also Read: Definition and Types of Customs Law and Trade Barriers

With duty structures understood, it is equally important to clarify roles and responsibilities under the Act.

Role and Responsibilities under the Customs Act 1962

The Customs Act defines the powers of customs officers and the obligations of exporters. Knowing this balance is essential for managing inspection risk and documentation accuracy.

What are the Responsibilities of a Customs Officer?

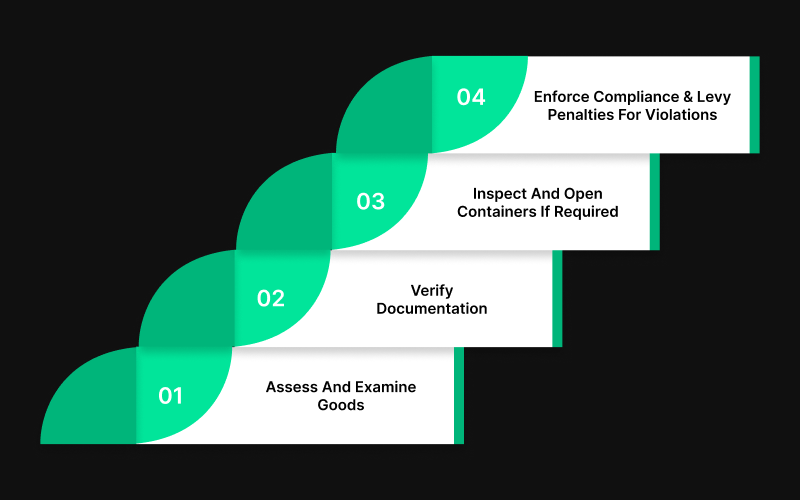

Customs officers are empowered to:

- Assess and examine goods

- Verify documentation

- Inspect and open containers if required

- Enforce compliance and levy penalties for violations

Their actions directly determine whether your shipment clears on time or is delayed. The Act gives them these powers to balance facilitation with enforcement.

Permissions and Licenses under the Customs Act 1962

Exporters must ensure they hold the right permissions and licences before engaging in cross-border shipments. These are often required before submission of customs filings:

- Import Export Code (IEC): Mandatory for export shipments

- Letter of Undertaking (LUT)/Bond: Used to export without paying IGST

- Shipping Bills and HSN Codes: Precise and accurate based on product specifications

Mistakes here often trigger compliance issues, rejection of refunds, or shipment holds, which may affect cash flow and buyer confidence. Proper internal checks and training on filing requirements help manage this risk.

Penalties and Offenses under the Act

The Act prescribes penalties for:

- Misdeclaration of value or quantity

- Wrong classification

- Attempted export of prohibited goods

- Non-compliance with the conditions of export schemes

Penalties can include fines, confiscation, and prosecution in severe cases.

Many exporters assume penalties apply only to deliberate fraud. However, even negligence can trigger monetary consequences.

Given this enforcement framework, recent amendments to the Act have further shaped exporter responsibilities.

Recent Amendments and Key Updates in the Customs Act 1962

The Customs Act evolves over time to adapt to changing trade dynamics and digital process reforms.

Recent updates affecting exporters include:

- Section 18A — Voluntary Revision: Allows businesses to revise customs filings to correct errors before enforcement actions. This reduces litigation risk and delays, as exporters can correct entries proactively.

- Provisional Assessment Time Limits: Introducing timelines for completing provisional assessments (e.g., 2-year limit) ensures clearance doesn’t drag indefinitely.

- Settlement Mechanism Changes: Functions previously under the Settlement Commission are being moved to interim boards to streamline dispute resolution.

- Advance Ruling Validity Extended: Amendments propose to extend the validity of advance customs rulings on classification and valuation from 3 to 5 years, reducing the frequency of re-application for recurring product lines.

These changes show that compliance is now data-monitored rather than solely inspection-based. This directly influences how exporters plan shipments.

How Does the Customs Act 1962 Influence International Trade

The Customs Act affects more than legal compliance; it impacts shipment timelines, cost structures, buyer commitments, and commercial risk for Indian exporters. Below are the key operational effects:

- Clearance Timelines and Shipment Flow: Delays in assessment or documentation queries can hold goods at Customs, pushing cargo beyond cut-offs and causing vessel rollover charges.

- Risk of Physical Examination: Shipments flagged by RMS or inconsistent declarations may face physical checks, adding days to clearance and complicating schedule planning.

- Buyer Delivery Commitments: Exporters with tight buyer timelines face commercial consequences when Customs clearance lags, affecting trust and future orders.

- Impact on Working Capital: Late GST/IGST refunds or unresolved provisional assessments tie up capital, reducing cash flow available for subsequent shipments.

- Penalty and Compliance Liability: Misdeclaration, valuation errors, or incentive irregularities can lead to penalty notices that increase landed cost and contractual exposure.

- Commercial Cost of Detentions: Container detention, port storage, or re-shipping costs arising from Customs holds directly erode margins, especially in time-sensitive trades.

- Contractual Exposure with Buyers: When clearance delays alter ETA, exporters may absorb costs under Incoterms and long-term contracts, impacting pricing strategy.

- Competitive Positioning in Global Markets: Consistent compliance and predictable clearance speeds help exporters quote reliable delivery schedules — a competitive advantage over inconsistent players.

- Demand for Documentation Accuracy: Digital faceless systems flag deviations quickly, requiring exporters to maintain precise invoices, classification, and valuation to avoid setbacks.

While the Act sets the legal foundation, exporters also need logistics coordination that aligns with customs processes. That is where operational support like Pazago becomes crucial.

How Pazago Simplifies Customs Compliance and Trade Operations

The Customs Act, 1962, places exporters under constant pressure to get shipping documents, classification, duty filings, and compliance right every time. Errors here cost time, money, and buyer trust.

Pazago supports Indian exporters by reducing logistics-linked compliance disruptions and improving shipment control in the following ways.

- Logistics planning aligned with the Customs Act 1962 requirements: With customs filings closely linked to operational readiness, Pazago helps exporters align cargo readiness, container movement, and vessel schedules with these timelines so documentation processes and shipment movement stay coordinated.

- Assured container booking and loading coordination: Even if customs clearance is granted, container unavailability or loading misalignment can cause rollover. Pazago confirms container allocation and coordinates factory-to-port movement so that clearance and vessel schedules remain aligned.

- Daily Status Reports for shipment visibility: Under data-driven customs systems, shipment movement updates become critical. Pazago provides Daily Status Reports covering container movement, vessel ETD/ETA updates, and documentation status.

- Support across exporter scale: Whether handling a single LCL shipment or multiple FCL containers, exporters receive structured coordination support. Smaller exporters often struggle with documentation follow-up and schedule monitoring; structured communication reduces oversight gaps.

By aligning logistics coordination with compliance timelines, Pazago helps exporters reduce uncertainty around customs clearance and shipment departure.

Conclusion

The Customs Act, 1962, remains the foundation of India’s cross-border trade regulation. It defines how goods are assessed, inspected, valued, and cleared. In 2026, digitisation, faceless assessment, and data-driven scrutiny have increased the importance of documentation accuracy and procedural discipline for Indian exporters.

Exporters who understand their responsibilities under the Act are better prepared to avoid detention, penalties, and unexpected delays. Staying updated on amendments, understanding duty implications, and maintaining documentation discipline reduces operational risk.

If your export operations require tighter control across booking, documentation alignment, and shipment tracking under the Customs Act 1962 framework, Pazago can support you with structured logistics coordination built around exporter realities. Contact us today.

FAQs

1. What is the Bill of Entry and its filing requirements?

A Bill of Entry is a customs declaration filed by an importer under the Customs Act, 1962, for clearance of imported goods. It includes details of goods, value, classification, and duty payable. It must be filed electronically before or upon the arrival of goods, within prescribed timelines.

2. What are the main definitions in Section 2 of the Act?

Section 2 of the Customs Act, 1962 defines key terms such as “import,” “export,” “customs area,” “customs station,” “dutiable goods,” “prohibited goods,” and “baggage.” These definitions establish the legal scope of customs control, clarify liability, and guide interpretation and enforcement under the Act.

3. What are 'dutiable goods' and how is it determined?

Under the Customs Act, 1962, “dutiable goods” are goods on which customs duty is leviable and not exempt. Determination depends on tariff classification, assessable value, applicable duty rates under the Customs Tariff, and any exemption notifications issued by the government.

4. Explain the concept of 'baggage' under the Act.

“Baggage” under the Customs Act, 1962, refers to personal belongings of passengers carried during travel. It includes accompanied and unaccompanied baggage but excludes goods imported for trade. Baggage is subject to specific duty rules, allowances, and declarations at customs checkpoints.

5. What powers does the Central Board of Indirect Taxes and Customs (CBIC) hold?

The Central Board of Indirect Taxes and Customs administers customs laws under the Customs Act, 1962. It issues circulars, notifications, and regulations; oversees customs officers; grants exemptions; clarifies procedures; and ensures uniform implementation, enforcement, and collection of customs duties across India.