.png)

What Is Forex Management in Export Trade? A 2026 Guide for Indian Export Teams

Optimize your business: use unlimited savings with Pazago fulfilled now!

Get Started ->In 2026, more Indian exporters are testing new lanes and counterparties as talks such as the India–GCC FTA move forward. New lanes don’t just change routing—they change when you get paid, how long receivables stay open, and how much room the exchange rate has to move before realisation.

Forex management in export trade is the day-to-day discipline of tracking and controlling that exposure across contracts, documents, shipment milestones, and collection, so pricing assumptions and realised outcomes don’t drift apart.

This guide explains forex management in plain terms and shows how export teams can run it as a repeatable workflow, rather than treating FX as a one-off finance task.

Key Takeaways

- Forex management is how trade teams plan, track, and control currency exposure so realised margin and cash flow don’t drift.

- It shows up between quote/PO → shipment → invoice acceptance → collection, where timing changes can keep exposure open longer.

- Best practice: track open exposure by amount, currency, and due date at each milestone, in one place.

- Treat execution slippage (doc mismatches, approval delays, late remittance) as an FX risk driver, not “just ops noise.”

Forex Management Meaning for Indian Exporters

For an exporter, forex management means managing the currency exposure created by export receivables (and any exporter-side costs priced in foreign currency), so your realised margin and cash collection don’t drift between the day you quote and the day you receive funds.

It’s not about predicting the market. It’s about controlling the rate and timing risk that opens up across contract terms, documentation, dispatch, and collection.

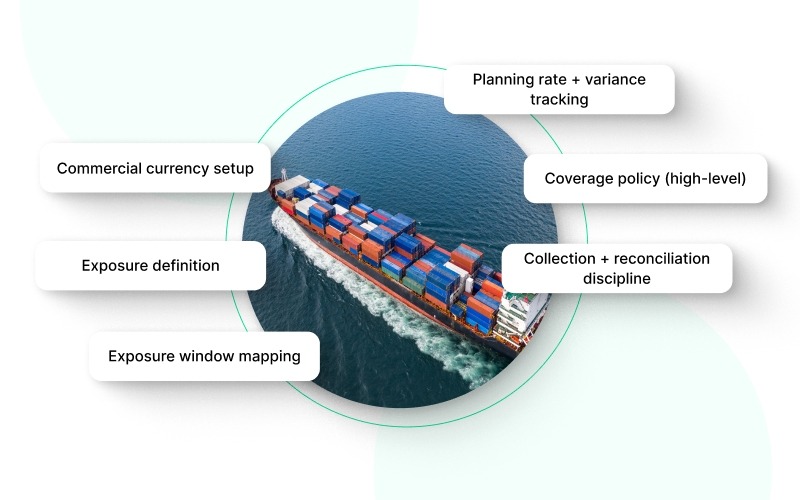

What Forex Management Covers

- Commercial currency setup: Quote and invoice currency choices, plus exporter-side costs in other currencies, so you know what’s fixed vs what can move.

- Exposure definition: Tying exposure to one source of truth (contract/PO value, invoice value, LC amount, or agreed settlement amount).

- Exposure window mapping: Clarifying when risk starts and ends (invoice date vs BL date vs document acceptance vs agreed credit period).

- Planning rate + variance tracking: Separating “rate impact” from “timing impact” when realisation differs from plan.

- Coverage policy (high-level): Rules for when rate protection is needed and who approves it, so decisions aren’t made under due-date pressure.

- Collection + reconciliation discipline: Handling partial receipts, deductions, and bank charges so realisation doesn’t end in unexplained gaps.

What Forex Management Is Not

It’s not FX trading, and it’s not “only hedging.” It’s the operating routine that keeps export exposure visible, controlled, and closed on time so the money you collect stays close to what you priced.

Where Forex Risk Shows Up in the Export Workflow

1. Quotation / Proforma → exposure is assumed, not owned yet → lock what can still move

At this stage, FX risk is still a pricing assumption: the rate you’re quoting versus the rate you may collect later.

Capture the quote currency, validity window, and any exporter-side costs sitting in other currencies (freight, insurance, inspection) so you know what’s fixed vs floating.

2. PO / Contract lock (Incoterms + payment terms) → exposure becomes real → define ownership and the “clock start”

Once the PO/contract is signed, the receivable exposure is real. Record the trade terms (what’s included in your price), the payment method and terms (advance / DP / DA / LC), and the trigger that starts the payment clock (invoice date, BL date, dispatch, delivery, or document acceptance).

3. Shipment readiness → timing slippage widens the window → track schedule drift early

When production readiness, pickup, gate-in, or vessel schedules move, the collection timeline often moves with it, even if the invoice value doesn’t.

Track ETD changes and milestone slippage that can push document handover and payment events later than planned.

4. Invoice + document finalisation → amount/date drift risk spikes → reconcile to the deal, not the draft

This is where avoidable variance enters: short shipment adjustments, revised charges, credit/debit notes, or late edits that change the final invoice value or the effective due date.

Compare invoice currency/amount to the PO/contract and flag anything that could delay document acceptance by the buyer/bank.

5. Payment/settlement → the rate becomes real → capture value date and net credit

FX outcome locks when money actually lands (or is converted), not when you send the invoice. Capture the value date, whether receipts are partial, any bank fees/deductions, and whether the collection slipped past the planned due date.

6. Realisation + reconciliation → variance becomes visible → tag the driver so it doesn’t repeat

When you reconcile receipts back to the invoice and your planned rate, classify what caused the variance: rate movement, timing drift, amount drift, or acceptance/document delay.

This tells you whether the fix is commercial (terms), operational (milestones/docs), or treasury (rate coverage policy).

Exporter takeaway: Forex risk is felt at realisation, the gap between what you priced and what you finally collect, driven as much by execution timing as by the rate itself.

These decisions are simple enough for leadership to approve, and practical enough for ops and finance to run without daily firefighting.

The 5 Decisions That Keep Realisation Predictable

Once you’ve mapped where forex risk shows up in the export workflow, the next move is to lock a few operating rules that stop the “rate + timing” problem from drifting quietly in the background.

These aren’t treasury concepts. They’re practical decisions export teams can run every cycle, so pricing assumptions, due dates, and collections stay aligned from quote to realisation.

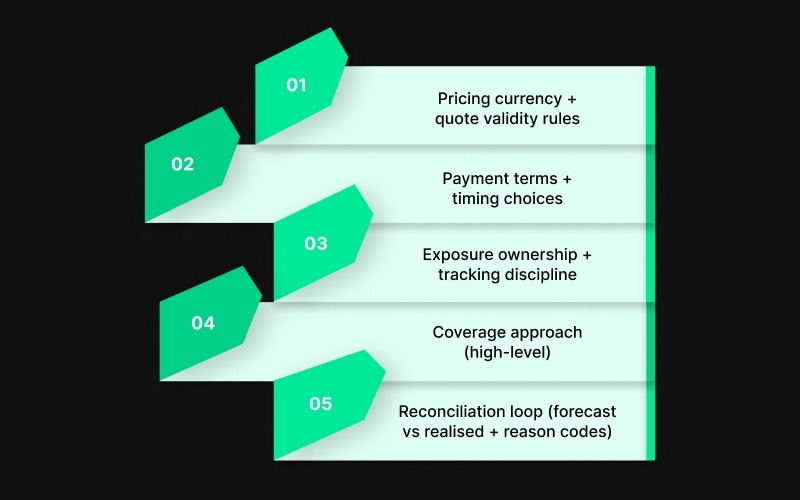

1) Pricing currency + quote validity rules

Decide: Which currency you quote and invoice in, and what rate assumption you’re using for commercial approval.

Lock: A clear quote validity window, plus explicit re-quote triggers (time elapsed, a defined rate move, or a shipment/dispatch delay).

Common failure: Quotes stay “live” while dispatch or payment timelines slip, and pricing never gets re-approved.

Simple rule: If the timeline crosses your validity window, route it through fresh commercial approval.

2) Payment terms + timing choices

Decide: Terms that define when cash is expected, not just whether payment is “secure.”

Lock: The exact trigger that starts the clock (invoice date/BL date/dispatch/document acceptance/delivery) and the credit period that follows.

Common failure: Teams assume the due date from memory, while the contract trigger says otherwise.

Simple rule: Write the trigger in the tracker exactly as the contract states it, then calculate the due date from that.

3) Exposure ownership + tracking discipline

Decide: Who owns exposure tracking and how often it’s updated.

Lock: One tracker, one owner, and one update cadence (weekly or milestone-based).

Common failure: Ops and finance work off different dates/amounts and only reconcile at month-end.

Simple rule: Any milestone change that shifts date or amount updates the exposure line item the same day.

4) Coverage approach (high-level)

Decide: When exposure stays open versus when rate protection is applied, based on policy not mood near collection.

Lock: Approval thresholds (value, margin sensitivity, tenor) and who approves.

Common failure: Dates drift, escalation doesn’t happen, and decisions get forced late.

Simple rule: Tie the coverage decision to the moment exposure is confirmed, with an escalation trigger if dates move.

5) Reconciliation loop (forecast vs realised + reason codes)

Decide: How the variance will be explained so it reduces over time.

Lock: Reason codes that separate rate movement, timing drift, vs amount drift, vs doc/acceptance delay.

Common failure: “FX gain/loss” gets logged, but the operational cause never gets fixed.

Simple rule: Don’t close variance until it has a reason code and an owner action for the next cycle.

These decisions only work if they show up in a routine your ops and finance teams actually follow.

A Simple Forex Management Workflow Per Shipment or Monthly

Use this as a repeatable routine. The goal isn’t perfection. The goal is one clear view of what’s open, what changed, and what you’re doing about it.

1) List exposures

- Capture every open export receivable (and any exporter-side costs in foreign currency, if relevant).

- Log: currency, amount, counterparty, expected collection date, and the contract trigger behind that date.

- Tie each item to one source of truth (contract/PO, invoice, LC, or agreed settlement amount).

2) Apply guardrails

- Set one planning rate for forecasting and pricing reference.

- Define escalation triggers (timeline slip, value threshold, or margin buffer getting thin).

- Confirm who reviews exposures and how often (weekly or milestone-based).

3) Choose coverage action (per policy)

- Use your policy to decide: leave open, cover partially, or cover fully.

- Record the decision owner and decision date so it’s auditable later.

- If dates shift beyond your escalation trigger, force a review instead of letting it ride.

4) Track changes (date/amount drift + change reason)

- Update the exposure line item whenever a milestone changes the expected collection date or amount.

- Tag the change reason (schedule change, document delay, buyer/bank acceptance delay, partial receipt, invoice revision).

- Keep the entry current enough that ops and finance are looking at the same “today view,” not last week’s plan.

5) Close + learn (variance → fix upstream)

- Close the exposure with the value date and net credit received.

- Classify variance using your reason code (rate movement, timing drift, amount drift, doc/acceptance delay).

- Assign one owner action that prevents a repeat (terms tweak, earlier escalation, document control, milestone discipline).

When this routine isn’t followed consistently, the cracks show up in the same places every time: timing drift and handoffs.

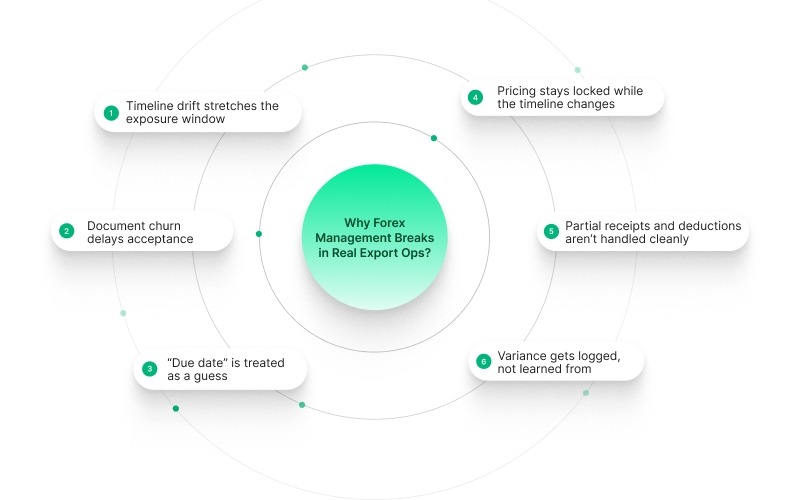

Why Forex Management Breaks in Real Export Ops

Most FX variance shows up after timelines and document acceptance drift, when the receivable stays open longer than the quote assumed.

- Timeline drift stretches the exposure window → ETD rolls, gate-in shifts, sailing changes, and the collection date quietly move out, leaving your planned rate assumption outdated.

- Document churn delays acceptance → a mismatch or late edit holds up document acceptance, so payment triggers later than expected.

- “Due date” is treated as a guess → teams remember “30 days” but ignore what starts the clock (BL date vs invoice date vs document acceptance).

- Pricing stays locked while the timeline changes → dispatch slips, but the quote validity and re-approval rule isn’t triggered, so margin risk is carried silently.

- Partial receipts and deductions aren’t handled cleanly → bank charges, short receipts, or split remittance create gaps that get labelled “FX” even when it’s an execution issue.

- Variance gets logged, not learned from → “gain/loss” is recorded, but the reason code and corrective action never loop back into terms, docs, or milestone discipline.

This is where execution control matters; when shipment milestones, documentation, and updates stay aligned, your FX tracker stops changing under your feet.

How Pazago Helps Export Teams Reduce FX Surprises by Controlling Shipment Drift

Forex planning only holds when shipment milestones and document acceptance dates hold. When ETDs roll, gate-in slips, or BL/document loops get stuck, the receivable stays open longer, and realisation starts drifting from what the quote assumed.

1. More stable shipment milestones, so the exposure window doesn’t keep stretching

Export issue: Rollovers, missed gate-ins, or pickup slippage push ETDs and delay the chain of events that lead to collection.

How Pazago helps: Booking follow-ups and milestone-led coordination across factory/CFS/port handoffs so schedule shifts surface early, and teams can act in time.

Why it matters for forex management: fewer “silent extensions” that keep exposure open past the commercial validity window.

2. Cleaner documentation movement, so payment triggers don’t get pushed out

Export issue: Document mismatches and late fixes delay buyer/bank acceptance, shifting the effective due date.

How Pazago helps: Hands-on support across pre- and post-shipment coordination, including BL process support and issue follow-ups that keep the document loop moving.

Why it matters for forex management: fewer acceptance delays that distort collection timing.

3. Daily visibility, so ops + finance update the tracker from the same reality

Export issue: Updates scattered across threads create stale ETDs/ETAs and late escalations.

How Pazago helps: Daily Status Reports with movement updates, ETD/ETA shifts, transshipment changes, and BL status.

Why it matters for forex management: faster alignment on what changed and whether exposure needs review.

If your FX variance is often driven by shifting shipment dates or late document acceptance, Pazago can review your lane workflow and highlight where drift enters and where tighter coordination and visibility can reduce surprises.

Conclusion

Forex management meaning, for Indian export teams, is simple: keep currency exposure visible and controlled so the amount you finally realise stays close to what you priced. Risk doesn’t appear at one single point; it builds across quotes, shipment timelines, document acceptance, and collection timing.

The practical way to reduce surprises is to set clear commercial rules early, track open exposure with ownership, and prevent timeline and documentation drift from stretching the window between invoice and realisation.

FAQs

1) Is forex management only hedging?

No. Hedging can be one tool, but forex management is broader: it’s how you define exposure, control timing, and explain variance so the same surprises don’t repeat. Many exporters improve outcomes just by tightening dates, ownership, and document discipline.

2) What creates bigger FX surprises: rate moves or delays?

Often delays. When dispatching, document acceptance, or remittance slips, your exposure stays open longer, giving the rate more time to move and pushing realisation away from the plan. Rate movement hurts most when timelines drift quietly.

3) Does invoicing in INR remove forex risk?

Not always. You may reduce currency exposure on the receivable, but risk can still sit in exporter-side costs priced in foreign currency, contract clauses that reference foreign currency, or payment structures where timing and deductions still change the net amount realised.

4) What should teams track first: amount or due date?

Due date. Amount matters, but timing decides how long exposure stays open and whether your planning assumptions still hold. If the due date shifts, the same invoice value can produce a very different realised outcome.

5) One internal control that reduces FX surprises fast?

A single exposure owner with a single tracker that must be updated whenever a shipment or document milestone shifts. Most “FX surprises” start as small date/acceptance changes that nobody captures until the month-end close.