.png)

Inland & Ocean Marine Insurance: Which is Right For You?

Optimize your business: use unlimited savings with Pazago fulfilled now!

Get Started ->When you’re an Indian exporter, moving goods across borders isn’t as simple as booking a container and waiting for it to arrive. Every shipment carries a bundle of risks that could threaten your buyer relationships and bottom line, especially during transit.

It might be a mishap during inland transport or a storm at sea; damage, delays, and unexpected costs are part of the game. You have invested time, effort, and money in securing the best deals, but without the right insurance, those efforts can quickly unravel.

When you have both options: Inland marine and ocean marine insurance are available, which one will you choose? To understand it, follow this guide till the end and know what you need to know to protect your shipments, and ultimately, your business.

Key Takeaways

- Inland marine insurance is essential for protecting goods during land-based transit and temporary storage, covering risks like theft, accidents, and mishandling.

- Ocean marine insurance covers goods during their ocean transit, protecting against risks like storms, piracy, and damage caused by jettison or stranding.

- Common mistakes include assuming inland risks are covered by ocean policies or choosing minimal freight contracts without adequate insurance for inland transit.

- Choosing the right insurance depends on the stage of transit your goods are in and the risks involved.

- Inland marine insurance is needed before the ocean shipping phase, while ocean marine insurance takes over once goods are aboard a vessel.

What Indian Exporters Should Know About Transit Risks?

As an Indian exporter, you are well aware of the complexities involved in moving goods from your factory to your buyer across international borders. The journey is long, and risks lurk at every stage.

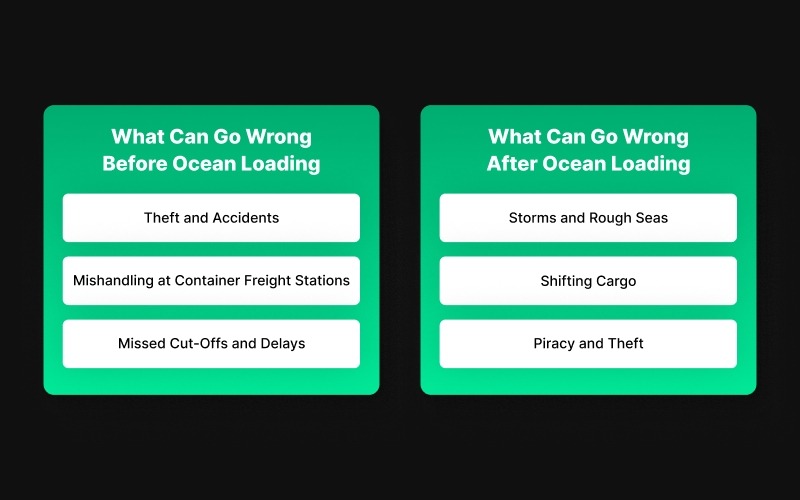

What Can Go Wrong Before Ocean Loading

The first part of the journey often happens before your goods even get to the ocean.

- Theft and Accidents: Trucks can be hijacked, or goods might be damaged in accidents along the way. This is especially true if you're shipping high-value or fragile items.

- Mishandling at Container Freight Stations (CFS): Cargo is often handled multiple times at various consolidation and forwarding stations. A mistake at any of these points, such as incorrect loading, poor sealing, or documentation errors, can lead to issues.

- Missed Cut-Offs and Delays: Relying on your initial Estimated Time of Departure (ETD) can be dangerous. If there are delays at the CFS or unforeseen roadblocks, you might miss vital shipping windows, affecting your buyer’s timeline.

What Can Go Wrong After Ocean Loading

Once your goods are safely loaded onto a container ship, you might think the worst is behind you. But ocean transit comes with its own set of risks.

- Storms and Rough Seas: Bad weather can cause significant delays, damage, or even the loss of cargo. While you may have a clear plan for shipping, weather-related events are unpredictable and outside your control.

- Shifting Cargo: Improperly packed or poorly secured goods can shift during transit, leading to damage. The risk is greater with long shipments, where goods are in transit for weeks or even months.

- Piracy and Theft: Depending on your shipping route, piracy can be a genuine concern. Certain regions, particularly off the coast of Africa and Southeast Asia, are known for piracy attacks, and if your goods are caught in one, recovery can be a lengthy and expensive process.

These are the reasons why the absence of this coverage leaves you vulnerable, potentially resulting in significant financial losses. So, you need to understand insurance in detail, one by one.

Also Read: Key Functions and Importance of Logistics Management

Detailed Explanation of Inland Marine and Ocean Marine Insurance

When you’re exporting goods internationally, the journey doesn’t end at the factory door. From the moment your products leave your warehouse to the time they reach their overseas buyers, there are a multitude of risks at every stage.

Inland marine and ocean marine insurance are two critical types of coverage that ensure your goods stay safe during transit. Let’s understand the details and make sure your goods are protected every step of the way:

Inland Marine Insurance

Inland marine insurance provides protection for goods that are in transit or temporarily stored off-site. Here’s a breakdown of the coverage:

- Property in Transit: Inland marine insurance covers goods while they are in transit over land, rail, or air.

- Mobile Equipment: If your business relies on specialised mobile equipment, this insurance will cover those assets when they are being moved between sites or used off-site. It ensures that even high-value machinery is financially protected during transport.

- Off-site or Temporary Storage: Inland marine insurance is not limited to transit; it extends coverage to goods temporarily stored at locations like warehouses, exhibitions, or job sites. This is vital for businesses with items frequently stored before they are shipped or used, as it protects against risks like theft, fire, or other losses during storage.

- Bailee Coverage: For businesses that store, repair, or handle client property (such as repair shops, dry cleaners, and storage facilities), bailee coverage is included. This protects against loss or damage to client-owned items that are in your care or custody, which is common in industries handling third-party goods.

- Specialised Equipment Coverage: For industries with high-value or sensitive equipment, like fine art galleries and scientific tools, specialised inland marine policies can cover these items while in transit or temporary storage. This protection ensures that valuable items are safeguarded during their journey.

Where Indian Exporters Commonly Went Wrong

Many exporters make critical mistakes when choosing inland marine insurance. These common errors often stem from misunderstandings about what is covered and a failure to ask the right questions.

Many exporters settle for the minimal insurance included in standard freight contracts. However, these contracts often fail to cover the true scope of risks involved in inland transport, leaving your goods exposed to theft or damage without adequate protection.

What Exporters Must Ask Their Forwarder/Insurer

Here are some critical questions to ask your forwarder or insurer before purchasing:

- What Does the Coverage Include? Make sure you understand exactly which risks are covered during transit and at temporary storage points. Does the policy cover all modes of transport, such as trucks, trains, and air freight, or only specific types?

- What Are the Coverage Triggers? Ask when a claim will be triggered. Is it when goods are damaged, stolen, or lost during transit? Make sure you know exactly when you're entitled to claim.

- What Exclusions Apply? Request a clear list of exclusions, such as poor packing or undocumented handovers. Understand the fine print so you don’t get caught off guard by situations that aren’t covered.

Ocean Marine Insurance

Once your goods are loaded onto a ship, the risks of transit shift, and ocean marine insurance becomes essential. This type of insurance covers your cargo during the ocean phase of transit, protecting it from the perils it faces while at sea.

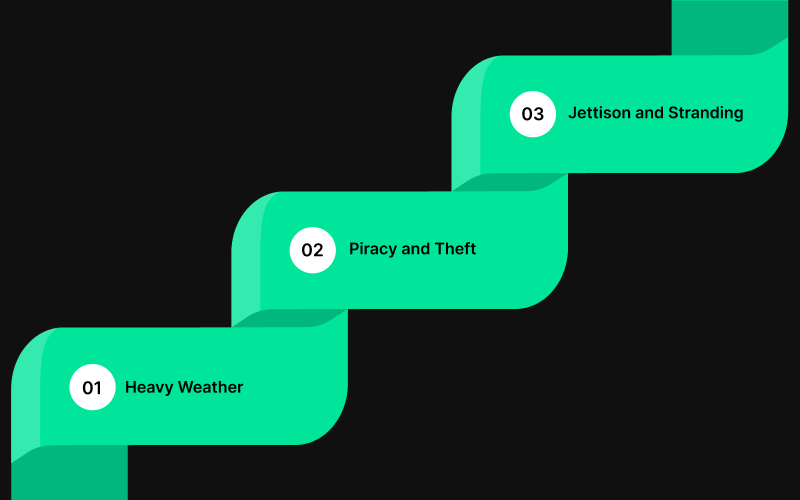

What Ocean Marine Insurance Covers

Ocean marine insurance provides coverage for a variety of maritime risks that can impact goods in transit:

- Heavy Weather: Covers damage to goods caused by storms or extreme weather conditions during the ocean voyage. Given the unpredictable nature of sea conditions, this is one of the most important aspects of ocean marine insurance.

- Piracy and Theft: Certain routes are prone to piracy, especially in high-risk regions. Ocean marine insurance protects against theft or hijacking of goods while they are at sea.

- Jettison and Stranding: If a ship encounters severe conditions, it may intentionally throw cargo overboard (jettison) or become stranded (e.g., running aground). Ocean marine insurance covers these kinds of risks to ensure that your goods are protected even in extreme situations.

Typical Gaps Exporters Overlook

While ocean marine insurance offers essential coverage, there are still gaps that many exporters overlook, leaving them vulnerable during transit:

- Transhipment-Related Risks: Goods are often transferred from one ship to another during their journey. This transhipment process can expose the goods to risks such as damage, loss, or theft. Many standard ocean marine policies do not automatically cover transhipment, so it’s important to ensure this is included.

- Delay in Notice of Loss/Ocean Bill of Lading Issuance: The Ocean Bill of Lading (OBL) is a key document that proves ownership and the terms of shipment. If the OBL is delayed or lost, your insurer may not accept the claim.

Ensure you understand the requirements and timelines for issuing the OBL to avoid claim rejections.

Here’s a quick overview of the differences between Inland Marine and Ocean Marine Insurance:

While both inland and ocean marine insurance are essential for protecting your goods, when to use each can significantly affect your costs, risks, and delivery timelines.

Also read: Essential Shipping Documents Every Importer and Exporter Should Know

How to Decide: Inland Marine or Ocean Marine?

Your cargo faces different risks on land than it does at sea. That's why choosing between Inland Marine and Ocean Marine insurance is about protecting your goods exactly where they need it most. Here's how to decide based on your shipment's specific route.

- For goods in transit before ocean shipping (whether overland or by air), inland marine insurance is critical. Without it, you risk not being covered for the numerous land-based risks like theft, accidents, and delays.

- Once goods are aboard a vessel or being shipped internationally, ocean marine insurance should take over to protect against sea-specific risks like rough weather, piracy, or jettison.

For the most effective protection, Indian exporters should ensure they have both types of coverage in place during different stages of the shipment process.

As your trusted logistics partner, Pazago goes beyond traditional freight forwarding by helping you provide proactive solutions to reduce risks.

How Pazago Helps Exporters Manage Insurance Risks

When it comes to managing risks during the shipment process, having the right insurance in place is only part of the solution. A logistics partner, such as Pazago, can proactively guide them through the process.

- Proactive Shipment Visibility: Through our daily status reports (DSRs) and real-time tracking updates, this platform ensures that you are always aware of your shipment's location and status.

- Mitigating Documentation Risks: This platform helps you stay on top of all documentation, from packing lists and bills of lading to HS codes, reducing the risk of errors that could invalidate insurance claims.

- Managing Transhipment Risks: Transhipment can introduce risks like damage or loss during the transfer between vessels. Pazago coordinates with your forwarder to ensure that your cargo is handled properly at every stage covered by insurance.

- Coordinating Risk Mitigation Strategies: Pazago’s expertise offers guidance on proper packing, handling, and transit practices to reduce the likelihood of damage, theft, or loss.

- Handling Post-Shipment Coordination: Our proactive approach ensures that if a problem occurs, it’s addressed quickly, minimising the impact on your shipment and buyer relationships.

Read Also: The Ultimate Guide to Feeder Vessels and Their Role in Global Shipping Routes

Conclusion

Inland marine and ocean marine insurance play crucial roles in ensuring the safe transit of goods for Indian exporters. By understanding the unique risks associated with both types of coverage, you can make informed decisions that protect your shipments and your bottom line.

However, securing the right insurance is just one piece of the puzzle. Having the right logistics partner to guide you through the complexities of transit and insurance is key to ensuring your goods arrive on time.

Pazago helps exporters coordinate shipments and maintain clear documentation, supporting smoother insurance processes when issues arise.

Contact us to learn how Pazago can help you coordinate export shipments with better visibility and operational control.

FAQs

1. What types of risks does inland marine insurance cover?

Inland marine insurance covers risks during the land-based transit of goods, such as theft, accidents, and damage during loading and unloading. It also provides protection for goods stored temporarily in off-site locations.

2. Can I get ocean marine insurance for goods in transit by air?

Ocean marine insurance primarily covers cargo transported by sea. For air shipments, exporters typically require air cargo insurance or a multimodal cargo policy that covers the entire transit route.

3. Does ocean marine insurance cover piracy?

Yes, ocean marine insurance covers risks associated with piracy, especially for shipments moving through high-risk areas. This protection is vital for exporters shipping goods through international waters.

4. How can I prevent delays caused by documentation issues during transit?

Ensure that all documents, including the bill of lading, packing list, and export compliance documents, are correct and complete before shipping. Keeping a close eye on deadlines and regularly verifying paperwork can prevent delays.

5. Are natural disasters covered by inland marine insurance?

Many inland marine policies can be customised to cover risks associated with natural disasters, like floods or earthquakes. However, this coverage may need to be specifically added as an add-on to your policy.