.png)

Transportation Charges Explained: A Practical Guide for Indian Exporters

Optimize your business: use unlimited savings with Pazago fulfilled now!

Get Started ->You've confirmed the order. The buyer is ready. Your goods are packed and ready to move. Then the freight quote lands in your inbox, filled with line items, ocean freight, origin charges, destination charges, and multiple surcharges.

You start scanning the numbers, only to realise you have no clear way to tell which charges are standard, which are negotiable, and which ones your buyer is actually supposed to absorb. You quote the buyer a CIF price and later discover you undercounted your transportation charges by ₹40,000 per container. Margin wiped out.

This scenario plays out regularly for Indian exporters, not because they're careless, but because transportation charges in international shipping are genuinely layered, inconsistently named across carriers, and rarely explained upfront.

This guide breaks down every major type of transportation charge Indian exporters face, what each one means in practice, and where the avoidable losses typically hide.

Key Takeaways

- Surcharges, origin handling, and inland haulage are routinely added to the base rate; never price exports based on freight alone.

- FOB, CIF, and CFR each shift transportation charge responsibility differently; misreading this means absorbing costs that were never yours.

- BAF, PSS, and congestion levies are active on most Indian trade lanes year-round. Always ask for a full breakdown of surcharges before booking.

- Trucking, OTHC, CFS handling, and CHA fees are recurring costs that must be modelled upfront, not discovered at shipment time.

- Knowing your complete transportation charges before you confirm a buyer price is the single most effective way to stop margin from leaking on every shipment.

Why Transportation Charges Are a Commercial Risk

Most exporters treat freight as a number provided by a forwarder quote. They compare it, accept it, and move on. But transportation charges are not a single number; they're a composite of multiple components, some fixed and some variable, some carrier-determined and some port-determined.

When you get a quote of $850 per 20-foot container on the India, Rotterdam lane, that number typically includes only the ocean freight component. The actual transportation charges you'll pay by the time the container is loaded and the bill of lading is issued can easily be 40–60% higher. If you've already committed to a buyer price under a CIF or CFR incoterm without accounting for this gap, the difference comes directly from your export revenue.

Understanding how Incoterms like CFR and CIF affect your cost responsibility is foundational, but knowing what's included in your total transportation charges is what actually protects your margins when you build export pricing.

Ocean Freight: The Base Rate That Changes Weekly

Ocean freight is the headline rate charged by a shipping line for moving your container from the port of loading to the port of discharge. For Indian exporters, this typically means a rate from JNPT (Nhava Sheva), Mundra, Chennai, or Kolkata to a destination port.

The problem isn't that ocean freight exists; it's that it's volatile and not guaranteed until a booking confirmation is issued. Spot rates on key lanes (India–Europe, India–US East Coast, India–Middle East) can shift by 20–30% within a single week during demand surges or supply-side disruptions. An exporter who quotes their buyer today using a rate from last week's enquiry can find that the actual freight has jumped significantly by the time they book.

The other common mistake: comparing quotes across carriers without realising that one carrier's "all-in" rate includes certain surcharges while another's base rate does not. You're not comparing like-for-like.

What to do: Always obtain a written booking confirmation of the freight rate validity before finalising buyer pricing. Never use verbal rates for commercial quotations. If your goods are volume-sensitive, say, you're shipping 20-foot vs 40-foot containers, the per-unit freight economics change considerably, so model both options.

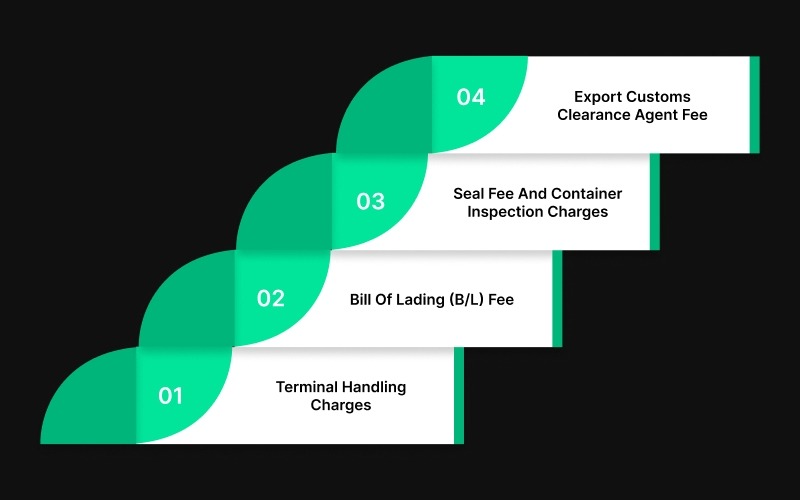

Origin Charges: What You Pay Before the Vessel Departs

Origin charges are transportation charges levied at the port of loading, in India, this means costs incurred before or at the time your container is handed over to the carrier. These are sometimes referred to as OBL charges or Origin Terminal Handling Charges (OTHC), and they are consistently underestimated by first-time exporters.

The main components under origin charges include:

- Terminal Handling Charges (THC / OTHC): Charged by the port terminal for receiving, storing, and loading your container onto the vessel. At JNPT, this is a regulated charge, but carriers may add their own documentation or handling fees on top of it.

- Bill of Lading (B/L) Fee: The carrier charges a fee to issue the Bill of Lading, the key document that gives you (and your buyer) title to the goods. This is typically between $50 and $100 per shipment, but varies by carrier.

- Seal Fee and Container Inspection Charges: Minor but real costs that add to your origin transportation charges.

- Export Customs Clearance Agent Fee: If you use a CHA (Customs House Agent), their fees are part of your origin-side logistics costs. Getting this wrong, or not accounting for it creates surprises at shipment time. The export customs clearance process involves specific documentation steps that your CHA navigates on your behalf, and their fees reflect that complexity.

Where exporters go wrong: Treating OTHC as if it's included in the ocean freight quote when it's not. Many carrier quotes explicitly state "excluding OTHC", and Indian exporters sometimes miss this disclaimer. On a 40-foot container shipped out of JNPT, OTHC alone can add $150–$250 to your total transportation charges.

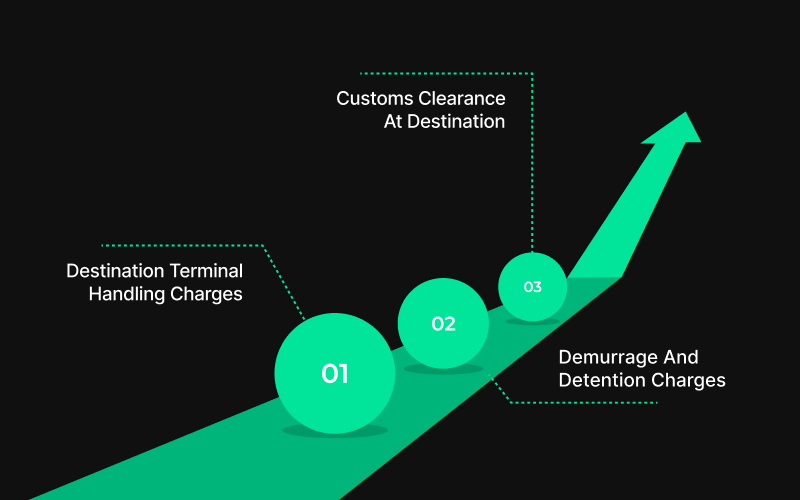

Destination Charges: The Costs Your Buyer May or May Not Own

Under FOB shipments, destination charges, everything that happens after the vessel departs from India, is the buyer's problem. But under CIF or CFR, you, as the Indian exporter, are responsible for freight and (under CIF) insurance to the destination port. Destination charges beyond the port are still the buyer's, but many exporters quote CIF without fully understanding where their liability ends and the buyer's begins.

Key destination-side transportation charges include:

Destination Terminal Handling Charges (DTHC)

Similar to OTHC, but charged at the discharge port. This is almost always the buyer's cost, but some carriers bundle it into their freight quotes in a way that can be confusing.

Demurrage and Detention Charges

These are among the most costly surprises in international shipping. Demurrage is the daily charge for keeping a container at the port beyond the free days allowed. Detention is for keeping the container outside the port beyond the free days. If your buyer in Germany or Dubai is slow to clear customs or pick up the goods, and the carrier's free days have expired, you or your buyer will be responsible for these charges.

Customs Clearance at Destination

Not technically your cost as a FOB or CIF seller past a certain point, but delays in destination customs clearance affect your buyer's satisfaction and your relationship with them.

The exporter's practical action here: Clearly document who is responsible for which transportation charges in your sales contract and on your invoice. Ambiguity about "who pays what at destination" leads to deductions from buyer payments and commercial friction.

To understand these cost boundaries more clearly, comparing EXW vs FOB incoterms and how each shifts responsibility for transportation charges is essential reading.

Also Read: What Causes Delivery Delays? 7 Strategies To Avoid Them

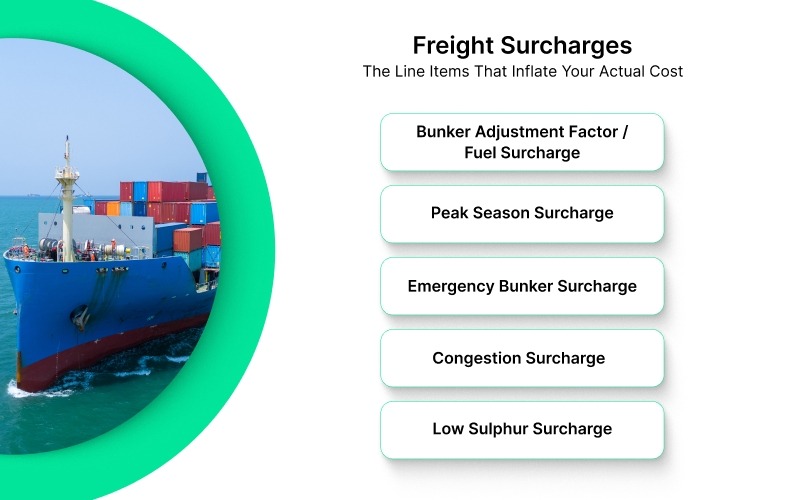

Freight Surcharges: The Line Items That Inflate Your Actual Cost

Surcharges are carrier-imposed additions to the base ocean freight that reflect real operational costs — fuel prices, congestion, peak demand, and route-specific risk factors. For Indian exporters, these transportation charges can add $200–$500 per container to the quoted base freight, sometimes more.

- Bunker Adjustment Factor (BAF) / Fuel Surcharge: Tied to global fuel prices. When oil prices rise, carriers pass this cost on as a surcharge. This is standard and unavoidable — but its amount varies, so always ask for the current BAF rate when getting quotes.

- Peak Season Surcharge (PSS): Carriers impose this during high-demand periods — typically pre-Christmas (October–December) for exports to Western markets, and Eid season for Middle East lanes. If you're exporting seasonal goods, factor this into your cost model.

- Emergency Bunker Surcharge (EBS): An additional fuel-related surcharge activated during sharp oil price spikes. Some lanes carry both BAF and EBS simultaneously.

- Congestion Surcharge: Activated at ports with container backlogs. In recent years, ports such as Los Angeles, Felixstowe, and even Colombo (a key transhipment hub for Indian exporters) have imposed congestion surcharges that added $100–$300 per container.

- Low Sulphur Surcharge (LSS): Related to IMO 2020 regulations on fuel sulphur content. Most carriers now include this in BAF, but some still list it separately.

The pattern here is clear: surcharges are real, recurring, and variable. An exporter who only tracks base ocean freight and ignores surcharges will consistently underprice their export shipments. The right approach is to ask your freight partner for a full surcharge breakdown at the time of booking, not after.

Inland Transportation Charges: The First and Last Mile Problem

A significant portion of total export logistics cost happens before the container reaches the port — and this inland leg is often quoted and managed informally, leaving room for cost overruns.

- Origin Inland Haulage (IHT)

The cost of trucking your goods from the factory or warehouse to the port. For exporters in Ludhiana, Coimbatore, Agra, or Rajkot, cities not directly on a major port, this cost can be $150–$400 per container, depending on distance, truck availability, and the weight of goods.

- Container Stuffing / CFS Charges

If you're using an LCL (less than container load) shipment or if you're stuffing at a Container Freight Station rather than at a factory, there are additional handling and stuffing charges that form part of your inland transportation charges.

- Port Congestion at Gate Entry

During peak export periods, trucks can wait hours at port gates, resulting in demurrage from the trucking company (detention at the gate). This is a real, under-discussed cost that shipment planning guides advise accounting for.

For exporters shipping under EXW terms, inland transportation is entirely your cost. For FOB exporters, it still falls on you until the goods are loaded on the vessel. Either way, it's a cost that needs to be modelled, not estimated loosely.

Also read: How to Book a Container for Export: Step-by-Step for First-Time Exporters

LCL vs FCL Transportation Charges: Choosing the Right Mode

When exporters casually compare LCL and FCL, they often look only at the headline freight rate. But the real difference shows up once all handling, documentation, and operational factors are taken into account.

Here’s a simple side-by-side comparison to make the cost structure clearer:

Air Freight Transportation Charges: When Speed Has a Price

Air freight works very differently from ocean freight. If you are not familiar with how airlines calculate charges, the final invoice can be much higher than expected.

Here’s a simplified breakdown exporters should keep in mind:

When Air Freight Is Used: Ideal for time-sensitive exports such as pharmaceutical samples, perishable foods, high-value electronics, and urgent replenishment orders.

How Charges Are Calculated: Billed on gross weight or volumetric (chargeable) weight, whichever is higher.

Volumetric Weight Formula: (Length × Width × Height in cm) ÷ 6000

Bulky but lightweight cargo can have volumetric weight 2–3x higher than actual weight.

Air Freight Rate: Charged per kg or per chargeable kg.

Common Additional Charges

- Fuel surcharge

- Security surcharge

- Airport handling charges (origin and destination)

- Airline documentation fees

Pricing Risk for Exporters: Exporters in textiles, handicrafts, auto components, and similar sectors should build a clear air vs. ocean freight comparison into their pricing to avoid absorbing urgent air shipment costs that buyers should cover.

How Pazago Helps Indian Exporters Manage Transportation Charges

Every section of this guide has pointed to the same underlying problem: transportation charges are fragmented, inconsistently communicated, and hard to plan around unless you have a logistics partner who gives you complete visibility upfront.

Here's where Pazago directly addresses these pain points:

- Competitive freight rates with cost predictability: Pazago provides Indian exporters with access to competitive ocean freight rates across major trade lanes, not just the base rate, but a complete cost picture that helps you price your exports accurately before committing to a buyer.

- Assured container booking and loading coordination: One of the most underappreciated risks in Indian export logistics is the gap between a freight quote and an actual confirmed booking. Pazago's assured container booking process closes this gap, so the transportation charges you plan for are the ones you actually pay.

- Pre-shipment and post-shipment support: From origin documentation to CHA coordination to managing origin-side transportation charges, Pazago's pre-shipment support reduces the friction that leads to cost surprises and delays. Post-shipment, the same team stays engaged to track your container and flag any issues before they escalate.

- Daily shipment status reports: The visibility gap during transit is a real commercial risk; buyers miss their commitments, and exporters can't accurately answer "where is my shipment?" Pazago's daily status updates give you the information you need to proactively manage buyer communication and delivery timelines.

- Support for exporters of all sizes: Whether you're a first-time exporter managing your first FCL shipment or an established SME running 30+ containers a month, Pazago's model is built to support Indian exporters without requiring minimum volumes or long-term contracts that limit your flexibility.

Transportation charges don't become simpler on their own. But with the right logistics partner, they become manageable and predictable enough to plan around.

Conclusion

Transportation charges are never just one number. They include origin handling, freight, surcharges, inland haulage, and destination costs. The gap between expected and actual costs is where export margins quietly shrink. That gap closes when you understand the full structure before committing to a buyer price.

Exporters who remain profitable are not always those with the lowest freight rates. They know which costs fall under their Incoterms. They factor in surcharges and origin expenses from the start. And they work with logistics partners who provide a complete cost picture upfront.

Every decision, from shipment planning to container selection and booking, links back to cost control and delivery reliability. Managing transportation charges carefully is how you protect your margins.

If you want predictable, transparent shipping costs without last-minute surprises, contact Pazago to see how structured freight planning can protect your export margins.

Frequently Asked Questions

1. What is the difference between ocean freight and total transportation charges?

Ocean freight is just the base rate charged by the shipping line for moving your container. Total transportation charges include origin handling (OTHC), surcharges, documentation fees, inland haulage, and insurance, which together can be 40–60% more than the base freight alone.

2. Which transportation charges does an Indian exporter pay under FOB terms?

Under FOB, the exporter is responsible for all costs up to and including loading the container onto the vessel at the Indian port. This covers inland haulage, CFS charges, customs clearance, and origin terminal handling. Everything from that point onward is the buyer's liability.

3. Why do freight surcharges keep changing, and how should exporters plan for them?

Surcharges like BAF and PSS are tied to fuel prices and seasonal demand, which fluctuate constantly. Exporters should always request a full surcharge breakdown at the time of booking and build a buffer into their export pricing rather than relying on last week's quote.

4. When does it make commercial sense to shift from LCL to FCL shipments?

Once your regular shipment volume consistently exceeds 10–12 CBM, FCL typically becomes more cost-effective as the per-unit transportation charges drop, and you gain better control over loading, transit time, and container condition.

5. Is marine cargo insurance mandatory for Indian exporters?

It is legally mandatory under CIF incoterms, where the exporter must arrange insurance to the destination port. Under FOB it isn't required, but most experienced exporters still take coverage; the premium is small relative to the financial exposure of an uninsured loss in transit.