.png)

Which Account Does Freight Come Under? Freight Accounting Guide for Exporters

Optimize your business: use unlimited savings with Pazago fulfilled now!

Get Started ->Freight costs are a regular part of every exporter’s expense sheet, yet few teams classify them correctly in accounts. Whether it’s the freight paid to bring goods into your warehouse or the cost of delivering shipments to buyers, each type affects your profit differently.

Misclassifying freight can distort your cost of goods sold (COGS), inflate expenses, and complicate audits. For exporters, these costs also influence export pricing, margins, and tax treatment.

In accounting terms, the question “freight comes in which account” depends on the direction of goods flow, inward or outward.

Understanding this difference helps you record transportation costs accurately, maintain clean books, and reflect the true profitability of your export operations.

Key Takeaways

- Freight classification depends on purpose. Freight-in (carriage inward) is part of inventory cost; freight-out (carriage outward) is a selling expense.

- Trade terms decide who records freight. Under FOB, buyers pay freight; under CIF, exporters bear it and record it as a selling expense.

- Accurate freight accounting protects margins. Correctly classifying freight ensures your COGS, profit, and GST filings are accurate and audit-ready.

- Pazago simplifies freight tracking. With centralised freight visibility, Pazago helps exporters reduce cost errors, link freight bills to shipments, and improve accounting accuracy across 110+ countries.

Freight in Accounts: Understanding Where Freight Costs Go

Freight is not always recorded under a single expense category. In accounting, it’s classified by purpose, whether it supports buying, producing, or selling goods. Each type of freight charge affects a different account and appears differently in your financial statements.

Freight-in (Carriage Inward)

Freight-in is the cost incurred to bring goods or materials to your business location. It is part of the cost of purchase, not a standalone expense.

- It is added to inventory cost and shown under Cost of Goods Sold (COGS) when goods are sold.

- For example, if you purchase raw materials worth ₹1,00,000 and pay ₹5,000 freight to deliver them to your warehouse, the total purchase cost becomes ₹1,05,000.

- In accounting entries:

- Dr Purchases (or Inventory) ₹1,05,000

- Cr Cash/Bank/Supplier ₹1,05,000

This reflects freight-in as a cost of acquiring goods, not a selling expense.

Freight-out (Carriage Outward)

Freight-out refers to the transportation costs you pay to deliver goods to customers.

- It is treated as a selling or distribution expense, recorded directly in the Profit and Loss (P&L) account.

- Example:

- Dr Freight Outward (Expense) ₹5,000

- Cr Cash/Bank ₹5,000

This approach separates freight-out from inventory costs, ensuring gross profit calculations stay accurate.

Effect of Shipping Terms (FOB/CIF)

Who records freight also depends on trade terms:

- FOB (Free on Board): Buyer bears freight cost once goods cross the port of shipment.

- CIF (Cost, Insurance, Freight): Seller bears freight cost and records it as an expense.

Understanding this distinction ensures your books match contractual obligations, critical in export accounting.

Also Read: Logistics and Freight Payment Software Solutions

Journal Entries for Freight Costs (Simplified for Exporters)

You can classify freight expenses into two main types: Freight-In (on purchases) and Freight-Out (on sales). Their accounting treatment differs based on purpose and trade terms.

Here’s a clear reference table:

This structure helps maintain consistency across transactions and ensures correct reporting for purchases, sales, and export shipments, without misclassifying freight between inventory and expense accounts.

Also Read: Analyzing Freight Charges and Rates in India

Freight Cost and Inventory Valuation Rules

Freight directly affects inventory valuation, how goods are valued in your books until sold. Incorrect classification can overstate or understate profit.

Freight Added to Inventory (Freight-In)

When freight is incurred to bring goods to your premises, it becomes part of the inventory’s purchase cost.

- Inventory value = Purchase price + Freight + Taxes (if non-recoverable).

- Shown under Assets → Current Assets → Inventory until goods are sold.

- When goods are sold, cost flows to COGS.

Example: Freight paid ₹5,000 on goods purchased for ₹1,00,000. Your inventory and cost of sales both reflect ₹1,05,000.

Freight Expensed Separately (Freight-Out)

Freight for dispatching goods to customers does not enhance asset value.

- It is a period expense, recorded when incurred.

- Shown under Operating Expenses → Selling & Distribution in the income statement.

Freight and Indian GST Context

Under GST, freight tax treatment depends on the service provider and contract structure. Exporters can generally claim Input Tax Credit (ITC) on eligible domestic freight services. Recording freight correctly supports GST reconciliation and audit readiness.

Also Read: Guide to Various Types of Freight and Shipping Charges

Freight Accounting for Export Transactions (Exporter Perspective)

Export freight accounting is shaped by contract terms and the responsibility for costs. How you record freight depends on who bears the charge, you (the exporter) or your buyer.

Getting this right ensures accurate profit recognition and compliance with trade documentation.

1. Freight under FOB (Free on Board)

- Under FOB, the buyer assumes responsibility for freight once the goods cross the export port.

- The exporter does not record freight as an expense.

- Freight invoices are billed directly to the buyer or their appointed forwarder.

- Only export sales and related documentation (commercial invoice, packing list, shipping bill) appear in the exporter’s books.

2. Freight under CIF (Cost, Insurance, Freight)

- Under CIF, the exporter arranges and pays freight and insurance.

- Freight cost is recorded as Freight Outward (Selling Expense).

- It is included in the export invoice value to the buyer, but shown separately in accounting books.

3. Freight Paid on Behalf of Buyer

Sometimes exporters pay freight on behalf of the buyer and recover it later. Record it as a receivable, not an expense:

Dr Buyer Account (Receivable)

Cr Cash / Bank

- When reimbursed, reverse the entry.

This maintains clear cost allocation and avoids distorting expense reports or profit margins.

Also Read: FOB vs CIF: What's The Difference? Which Is Better?

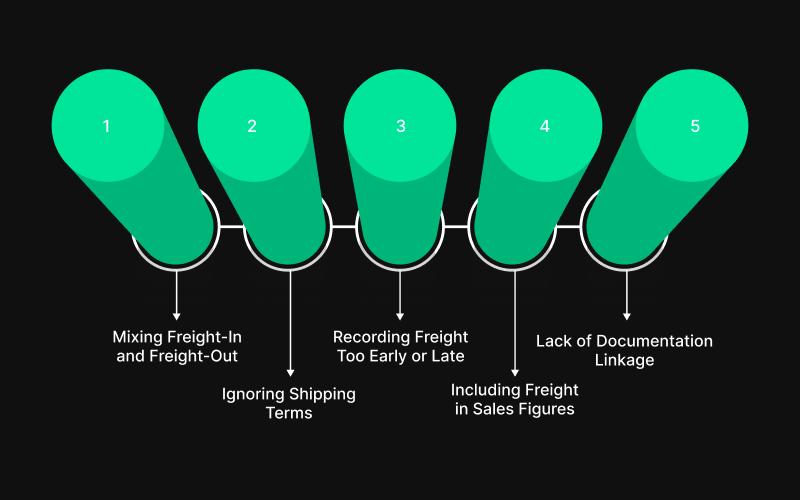

Common Mistakes in Freight Accounting and How to Avoid Them

Even experienced export teams make accounting errors with freight because shipping terms, documentation, and invoices vary by transaction. These mistakes can misstate profits or complicate audits.

1. Mixing Freight-In and Freight-Out

- Freight paid for purchases should be added to inventory (COGS).

- Freight for sales or exports should go to P&L as a selling expense.

Fix: Maintain two distinct ledger heads, Freight-Inward and Freight-Outward.

2. Ignoring Shipping Terms (FOB/CIF)

- Exporters often record all freight as their expense, even when buyers pay under FOB.

Fix: Check contractual terms and only record freight you are liable for.

3. Recording Freight Too Early or Late

- Recording freight before goods are received or shipped causes timing mismatches.

Fix: Record when risk or ownership transfers, typically at dispatch or delivery.

4. Including Freight in Sales Figures

- Some exporters add freight to sales instead of recording it separately.

Fix: Keep freight-out as an expense, not revenue, even if reimbursed later.

5. Lack of Documentation Linkage

- Freight invoices often lack cross-reference to order or shipment IDs.

Fix: Use structured export systems to link freight bills, orders, and shipments for audit clarity.

Practical Checklist for Accurate Freight Recording

Getting freight accounting right requires both precision and process discipline. Exporters who follow a structured workflow prevent misclassification, errors, and reconciliation delays.

Pre-Transaction Steps

- Confirm shipping terms (FOB, CIF, Ex-Works) before creating the invoice.

- Identify who pays freight: buyer, exporter, or freight forwarder.

- Match purchase or sales invoices with related freight documents.

Recording Stage

- Maintain separate ledgers for Freight-Inward (for goods purchased) and Freight-Outward (for goods sold).

- Verify that freight entries match the shipment reference numbers and container details.

- Record freight only when the service has been completed and the invoice received.

Post-Transaction Review

- Reconcile freight ledgers monthly with carrier statements.

- Review accrued freight payables for pending invoices.

- Cross-check freight data against GST filings and export documentation.

- Store all freight invoices with shipment documents for audit readiness.

Following this checklist ensures every rupee of freight is recorded under the right account, giving your finance team visibility over true landed costs and profit margins.

Also Read: Freight Optimization and Logistics Software

How Pazago Helps Exporters in Managing Freight and Export Logistics

Freight classification issues often stem from gaps in logistics execution rather than accounting errors. Rate volatility, unclear responsibility under FOB or CIF, last-minute container changes, and weak shipment visibility all make it harder to record freight correctly.

Pazago supports exporters at the logistics stage, where these problems begin.

Access Stable freight Pricing

By working closely with shipping lines, Pazago helps exporters access consistent freight rates across key routes, reducing last-minute price changes that complicate cost planning and freight accounting.

Confirmed container booking and loading coordination

Containers are secured in advance, with equipment release and loading coordinated at the factory, CFS, or port. This reduces rollovers, re-bookings, and unexpected freight adjustments.

Pre- and post-shipment support

Exporters receive continued coordination beyond booking, including documentation checks, BL follow-ups, and shipment-level support, ensuring freight responsibility stays clear throughout the export cycle.

Daily shipment visibility

Daily Status Reports (DSRs) provide updates on container movement, ETD/ETA changes, transshipments, and delays. This visibility helps teams align logistics activity with billing and accounting timelines.

Consistent support across exporter sizes

Whether handling a single LCL shipment or large container volumes, exporters receive the same level of attention and transparent coordination, reducing errors caused by fragmented communication.

By tightening control over freight execution and shipment visibility, Pazago helps exporters reduce delays, control costs, and maintain accurate freight records across international operations.

Conclusion

Freight costs can quietly impact your export profitability if not recorded accurately. By understanding whether they belong under inventory or operating expenses, you ensure that every shipment reflects its true cost and your books stay clean.

Clear freight accounting also strengthens audit readiness, GST compliance, and margin control.

Exporters who use structured systems like Pazago gain real-time visibility into logistics, freight, and documentation, helping them avoid errors and hidden costs that weaken cash flow.

Request a demo to see how Pazago's freight control and logistics management improves accuracy and transparency.

FAQs

1. Freight comes in which account?

Freight is charged to either Freight-Inward (part of purchase/inventory cost) or Freight-Outward (selling/distribution expense), depending on whether it relates to incoming or outgoing goods.

2. Is freight part of Cost of Goods Sold (COGS)?

Yes, Freight-In is added to COGS since it’s part of acquiring inventory. Freight-Out is not part of COGS; it’s recorded under selling expenses.

3. How is freight treated under FOB and CIF terms?

Under FOB, the buyer bears freight cost, so the exporter does not record it. Under CIF, the exporter pays freight, recorded as Freight Outward Expense.

4. Can freight be capitalised?

Only freight that directly brings goods or assets to a usable condition (like raw material delivery) is capitalised. Freight for sales or exports is expensed immediately.