.png)

Insurable Interest in Marine Insurance for Indian Exporters

Optimize your business: use unlimited savings with Pazago fulfilled now!

Get Started ->Your cargo was insured. The booking was confirmed. Documents were in place.

Yet when damage happened in transit, the insurer questioned whether you could actually claim.

For many exporters, claim disputes rarely arise from missing insurance. They arise from who legally bore the loss at the moment it occurred. A contract clause, title transfer, or in-transit sale can quietly shift that responsibility, leaving the exporter exposed even with an active policy.

Exporters should verify the delivery clause in the sales contract and the consignee in the Bill of Lading before dispatch.

This guide focuses on the situations where claims break down, how insurable interest changes during shipment, and what exporters must verify before dispatch so recovery does not depend on interpretation after the loss.

Key Takeaways

- Insurable interest in marine insurance is determined at the moment of damage, not when the policy was issued or paid for.

- Incoterms decide who bears the financial loss; arranging insurance does not automatically make the exporter the claimant.

- Ownership can shift during transit through document negotiation, resale, or contract terms, changing claim eligibility.

- Claims slow down when shipment timelines, BL endorsements, and payment records do not align.

- Cargo condition must be preserved until survey inspection, or insurers may question the cause and extent of damage.

What is an Insurable Interest in Marine Insurance?

In marine insurance, insurable interest means a financial stake in the cargo such that the insured party would suffer a financial loss if the cargo is damaged, lost, or delayed during transit.

Insurers assess this at the moment of loss. If your contract shows the risk had already shifted to another party, the claim may not be payable to you even though you arranged the insurance.

For exporters, this directly affects recovery and working capital. A rejected claim often turns into a commercial loss or a dispute with the buyer.

Why Does This Create Claim Disputes in Real Shipments?

During transit, ownership and risk frequently shift through Incoterms, document negotiation, or in-transit sales.

If the incident occurs after risk transfers to the buyer, the exporter may still hold the policy, but no longer hold the insurable interest. The insurer then questions claim eligibility.

Practical Rule Exporters Can Apply Before Dispatch

A claim generally holds only if both remain true at the time of damage:

- The sales contract shows that you still carried the shipment risk

- The loss impacts your finances, not only the buyer’s

Now the key question becomes when this interest actually exists during a shipment.

Also Read: What Causes Delivery Delays? 7 Strategies To Avoid Them

Incoterms & Ownership: Simple Rules Indian Exporters Must Follow

The key to successful marine insurance claims for Indian exporters is understanding when the financial responsibility shifts. In many cases, this shift happens at the moment defined by the Incoterms in the contract. Exporters must ensure that the insurable interest aligns with the risk they hold at the time of damage, or they risk claim rejection.

Here’s how to confirm risk transfer points and how to ensure the correct party receives the payout when a loss occurs:

1. FOB and CFR Shipments

In FOB (Free on Board), the exporter is responsible for delivering the goods to the vessel at the origin port. From that point onward, the buyer assumes responsibility for the shipment and its associated costs. The risk transfers once the goods are loaded, meaning the buyer’s insurance will cover any damage that occurs after that.

In CFR (Cost and Freight), the exporter pays freight to the destination port, but the buyer is responsible for arranging insurance because the risk transfers when the cargo is loaded on board.

Common Miscalculations:

- Exporters may purchase insurance “for safety” without verifying if the beneficiary (the buyer) is named correctly.

- Treating shipment arrival as the risk transfer moment, when it actually happens at loading.

- Quoting CIF price but contracting FOB terms, causing confusion about who bears risk.

- Assuming forwarder insurance automatically covers the exporter’s exposure.

What Exporters Should Confirm Before Loading:

- Ensure the Incoterm is clearly written in the sales contract (not just the proforma invoice).

- Confirm the named beneficiary on the insurance policy matches the party bearing the risk (the buyer in FOB).

- Make sure the coverage wording allows assignment if the risk transfers during the shipment.

- Verify the buyer’s awareness of their responsibility after loading (especially for FOB).

2. CIF and CIP Shipments

In CIF (Cost, Insurance, Freight) and CIP (Carriage and Insurance Paid To) contracts, the exporter arranges the insurance. However, the exporter is not automatically the claimant. The insurance is purchased for the buyer’s protection once the goods are shipped, so if damage occurs during transit, the loss typically falls on the buyer.

Exporters Should Verify:

- The policy wording allows the buyer to claim directly, especially in CIF or CIP contracts.

- That the coverage level matches the contractual obligation, ensuring the exporter isn’t underinsured.

3. Document Negotiation and In-Transit Sales

In Letter of Credit (LC) and Documents Against Payment (DP) transactions, ownership often moves when the documents are released by the bank, not when the goods arrive. From the insurer’s perspective, the risk shifts at the document release date, which means that even if the cargo is still in transit, financial exposure has already transferred to the buyer.

If an exporter ships machinery to Europe under LC terms, and the documents are released on Day 12 while the cargo is damaged on Day 19 during transshipment, the exporter may no longer be the party suffering the loss.

In the case of in-transit sales or contract amendments, the title transfers mid-voyage, and insurable interest follows the buyer unless the policy is assigned.

Required Action at the Time of Transfer:

- Notify the insurer immediately in writing.

- Endorse the policy beneficiary if necessary.

- Share the transfer timestamp with the bank and the buyer.

- Keep a record of acknowledgment.

4. DAP And Delivered Contracts

When delivery terms extend risk until arrival, the exporter retains exposure for a longer portion of the journey. Any incident during ocean transit, transhipment, or inland delivery may still affect the exporter financially.

Here, marine insurance directly protects the exporter’s working capital, and under-insurance becomes costly because the liability continues until delivery confirmation.

Exporters should check whether inland legs and handling stages are included in coverage and confirm the insurer recognises the extended responsibility.

Consider a shipment moving from Mumbai to Rotterdam under CIF terms. The exporter arranges insurance and sends documents through the bank. During transhipment, cargo damage occurs.

Once you know when the risk shifted, the next question is what financial stake remained with us. Before filing a claim, you must confirm which party is financially responsible for the shipment.

Read Also: Top 5 Marine Insurance Policy Providers In India

Types of Insurable Interest Exporters Deal With in Real Shipments

In marine insurance, interest is not limited to the cargo owner. Multiple parties around a shipment can legally claim financial loss, and insurers check which one applies before processing recovery.

For exporters, identifying the correct interest type decides:

- Who should be named in the policy

- Who receives claim proceeds

- Which documents will be requested

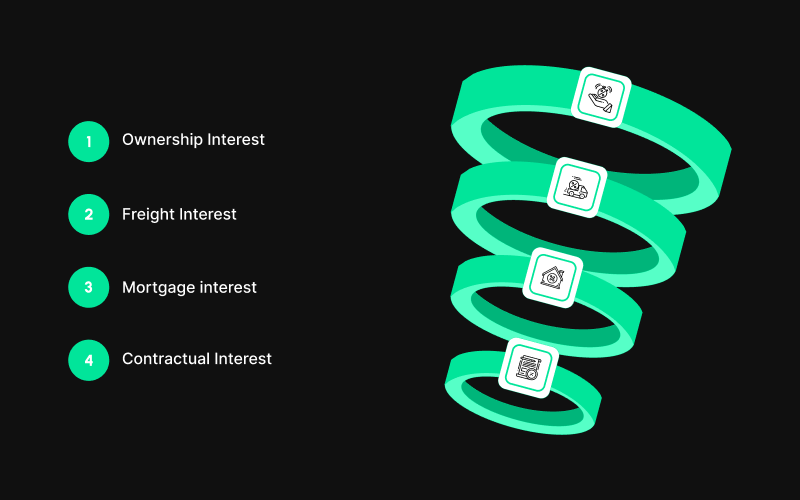

1. Ownership Interest

This applies when the exporter still legally owns the cargo at the time of damage.

Typical situations:

- Shipment under CIF/CIP before buyer risk transfer

- Goods not yet negotiated under the LC

- Payment pending while cargo is in transit

What insurers verify

- Commercial invoice

- Packing list

- Unendorsed bill of lading showing exporter as shipper

- Sales contract showing risk retained

2. Freight Interest

Sometimes the loss is not the cargo but the expected earnings from delivering it. This appears in exporter situations such as:

- Exporter responsible for delivering under certain contract obligations

- The exporter bears the cost of the replacement shipment

- Freight or logistics charges are recoverable only on successful delivery

What insurers verify

- Freight agreement

- Cost obligations in a sales contract

- Liability clauses

3. Mortgage interest

If goods are financed under LC, packing credit, or collateral arrangement, the lender holds a financial stake in the shipment.

In a loss event, insurers often require lender acknowledgement before settlement.

What insurers verify

- LC terms

- Bank charge or hypothecation clause

- Financing agreement

4. Contractual Interest

Even without ownership, a contract may make the exporter financially responsible. Examples exporters encounter:

- Quality replacement obligation

- Delivery guarantee clauses

- Charter or space commitment penalties

The exporter may need to compensate the buyer despite not owning the cargo at the time of loss.

What insurers verify

- Penalty clauses

- Delivery obligations

- Liability wording in the agreement

Once responsibility is clear, the practical question becomes how much of the loss the policy will actually pay.

Read Also: Understanding Ocean Shipping and Transport Services

How To Set The Insured Value So The Claim Covers The Real Loss?

If the loss fell on you, the next risk is the payout itself. Many claims do settle for less than expected because the insured value did not reflect the real exposure.

Insurers compensate the declared value at policy issuance. If that amount differs from the financial loss created by the incident, the shortfall stays with the exporter.

1. Market Value

This reflects the price the cargo would reasonably sell for at the time the insurance is arranged. It works when goods have stable pricing and immediate resale value. However, it may not represent contractual exposure if replacement cost or delivery obligations exceed market rate.

2. Replacement Cost

This reflects what it would cost to supply the buyer again after a loss. For exporters with delivery commitments, this often better represents actual exposure, since the commercial obligation continues even after damage during transit.

3. Agreed Value

Here, the exporter and insurer fix the value at the start of the policy. Claims rely on this pre-accepted figure rather than a later valuation. It avoids post-incident debate, but only if the agreed amount realistically matches shipment exposure.

Consider goods worth ₹50 lakh insured for ₹30 lakh. A 40% damage will not settle at 40% of ₹50 lakh. The settlement is calculated proportionately against the declared value. The uncovered portion becomes a working-capital loss.

Even when the contract terms and coverage look correct, recovery still depends on what the insurer verifies after the incident.

Also Read: Understanding Incoterms in International Trade

5 Common Claim Problems Exporters Face And How To Prevent Them

After the incident is reported and documents are reviewed, many claims slow down because the shipment was handled in a way that weakens proof. Insurers rely on sequence and evidence. When the operational record is unclear, the process shifts from settlement to verification.

Here's what you might face:

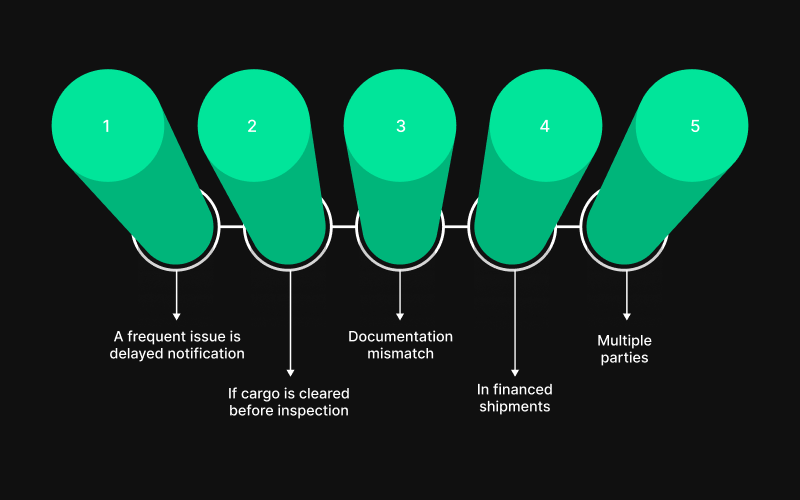

- A frequent issue is delayed notification. Exporters sometimes wait for confirmation from the buyer or forwarder before informing the insurer. During this gap, containers may be opened, cargo moved, or repacked.

Once the original condition is disturbed, the surveyor cannot reliably determine the cause or extent of damage, and recovery becomes uncertain. - If cargo is cleared before inspection, buyers often want quick delivery, and the shipment is released to avoid storage charges. Without the surveyor examining the cargo in its damaged state, insurers may question whether the loss occurred during transit or after handling at the destination.

- Documentation mismatch also creates disputes. The bill of lading, commercial invoice, and contract sometimes reflect different parties or dates. Even small inconsistencies suggest that financial responsibility may have changed before the incident, pushing the claim into clarification instead of settlement.

- In financed shipments, banks hold a financial interest. When they are not informed at the time of filing, insurers must confirm whether claim proceeds are payable to the exporter or lender. This coordination adds delay even after the damage assessment is complete.

- Multiple parties filing or guiding the claim simultaneously causes another slowdown. If the buyer, exporter, and forwarder communicate separately with the insurer, the insurer first establishes the correct claimant before continuing assessment.

When CIF shipments are booked, but insurance limits are not verified, exporters often discover that only minimum coverage was arranged. It might leave them to absorb the loss of the balance.

How Pazago Helps When Insurable Interest In Marine Insurance Affects Shipments

Uncertainty around insurable interest usually comes from not knowing exactly what changed during the shipment timeline. When these events are unclear, exporters struggle to reconstruct shipment timelines during claim reviews.

Pazago assists exporters at this point by improving how shipment operations are carried out through:

1. Continuous Shipment Visibility

Daily movement, departure, transhipment, and arrival updates help exporters track shipment stage changes and explain events accurately during claims.

2. End-to-End Coordination

Ongoing coordination after booking keeps loading status, document stages, and movement changes recorded, making responsibility easier to demonstrate.

3. Predictable Booking & Loading

Confirmed container planning and cut-off management reduce rollover-driven exposure and unintended delivery liability.

4. Clear Transit Communication

Regular updates enable timely responses to buyers on delays or cargo conditions, limiting later disputes during claim review.

By keeping shipment events documented and aligned, exporters can address insurance discussions with clear timelines instead of post-incident clarification.

Also Read: What Are The Differences Between FOB Shipping Point And FOB Destination?

Conclusion

Insurable interest in marine insurance determines who can recover the loss, not who arranged the shipment or purchased the policy. During export transactions, risk shifts through contract terms, document transfer, and delivery obligations. When exporters track only cargo movement but not financial responsibility, claims become uncertain even with valid coverage.

Clear contracts, accurate valuation, and consistent shipment updates keep recovery straightforward. Pazago supports exporters by improving execution visibility across the shipment lifecycle. Through confirmed booking coordination and regular shipment status reporting, exporters retain a clear operational record of shipment events.

This makes it easier to demonstrate responsibility and communicate accurately with buyers when incidents occur.

To maintain clear shipment records and reduce uncertainty during export incidents, contact Pazago to improve shipment coordination and operational visibility across your export logistics.

FAQs

1. Can an exporter still make a claim if the goods are sold during transit?

If the title of the goods has transferred to the buyer while in transit, the exporter may no longer hold insurable interest, and the claim would likely be directed to the buyer. However, if the insurance policy is assigned to the exporter, they may still be able to claim, depending on the contract and the timing of the sale.

2. What role does the bill of lading play in determining insurable interest?

The Bill of Lading helps indicate who holds title to the cargo, but risk transfer is determined by the sales contract and Incoterms. Exporters must ensure the Bill of Lading accurately reflects the party with insurable interest at the time of shipment damage.

3. What can exporters do if their claim is denied due to a lack of insurable interest?

If a claim is denied due to the insurer’s assessment of insurable interest, exporters should review the terms of the sales contract, the Incoterms used, and the documentation provided. They should consult with legal experts or their insurer to clarify the situation and explore options such as reassigning the policy or challenging the decision.

4. What are the implications of incorrect or incomplete documentation when filing a claim?

Incorrect or incomplete documentation can delay the claims process and possibly lead to denial. Exporters should ensure that all documents, including the Bill of Lading, commercial invoice, packing list, and insurance policy, match in terms of dates, ownership, and risk transfer details.