.png)

Customs Charges in India: Types, Calculation & When They Apply

Optimize your business: use unlimited savings with Pazago fulfilled now!

Get Started ->There's a shipment of automotive parts heading to Germany. Your production costs are locked, your buyer is ready, and then customs charges appear in your cost sheet. Suddenly, your carefully planned margins look different.

This happens more often than it should. Many exporters treat customs charges in India as an afterthought, only to discover they've miscalculated their landed costs or missed exemptions that could have saved them thousands of rupees.

Understanding customs charges isn't just about bureaucratic compliance; it's about protecting your pricing strategy, maintaining healthy margins, and avoiding the dreaded shipment delays that damage buyer relationships. Whether you're importing machinery for your production unit or exporting finished goods globally, customs charges in India directly shape your competitiveness.

This guide breaks down every customs charge you'll encounter as an Indian exporter, shows you exactly how calculations work with real examples, and helps you understand when these charges apply to your operations.

Key Takeaways

- Customs charges in India include multiple components: Basic Customs Duty (BCD), IGST, Social Welfare Surcharge (SWS), and protective duties, each serving a different regulatory purpose.

- BCD rates vary from 0% to 150% based on HSN codes, whilst IGST (applied on assessable value plus BCD) offers Input Tax Credit for registered businesses.

- Export duties are the exception in India's trade policy, applying primarily to minerals, raw hides, and select agricultural products during domestic shortages.

- Accurate HSN code classification is critical; a wrong code can mean the difference between 5% and 15% duty, directly impacting your landed costs.

- Free Trade Agreements can eliminate or reduce Basic Customs Duty on qualifying goods, whilst schemes such as Advance Authorisation and EPCG allow duty-free imports for export production.

What Are Customs Charges in India?

Customs charges are taxes and duties levied by the Government of India on goods entering or leaving the country. These charges serve multiple purposes: generating revenue for the government, protecting domestic industries from unfair competition, and regulating the flow of certain goods across borders.

When you import goods into India, you're required to pay these charges before your shipment clears customs. The same applies to certain export scenarios, though India's export policy is generally more favourable to encourage international trade.

Here's what makes customs charges in India particularly important for exporters: even though you're primarily moving goods out of the country, you often need to import raw materials, machinery, or components first. Every rupee you pay on imports affects your final product cost and export competitiveness.

Must Read: Essential Documents Required for Smooth Import-Export Customs Clearance

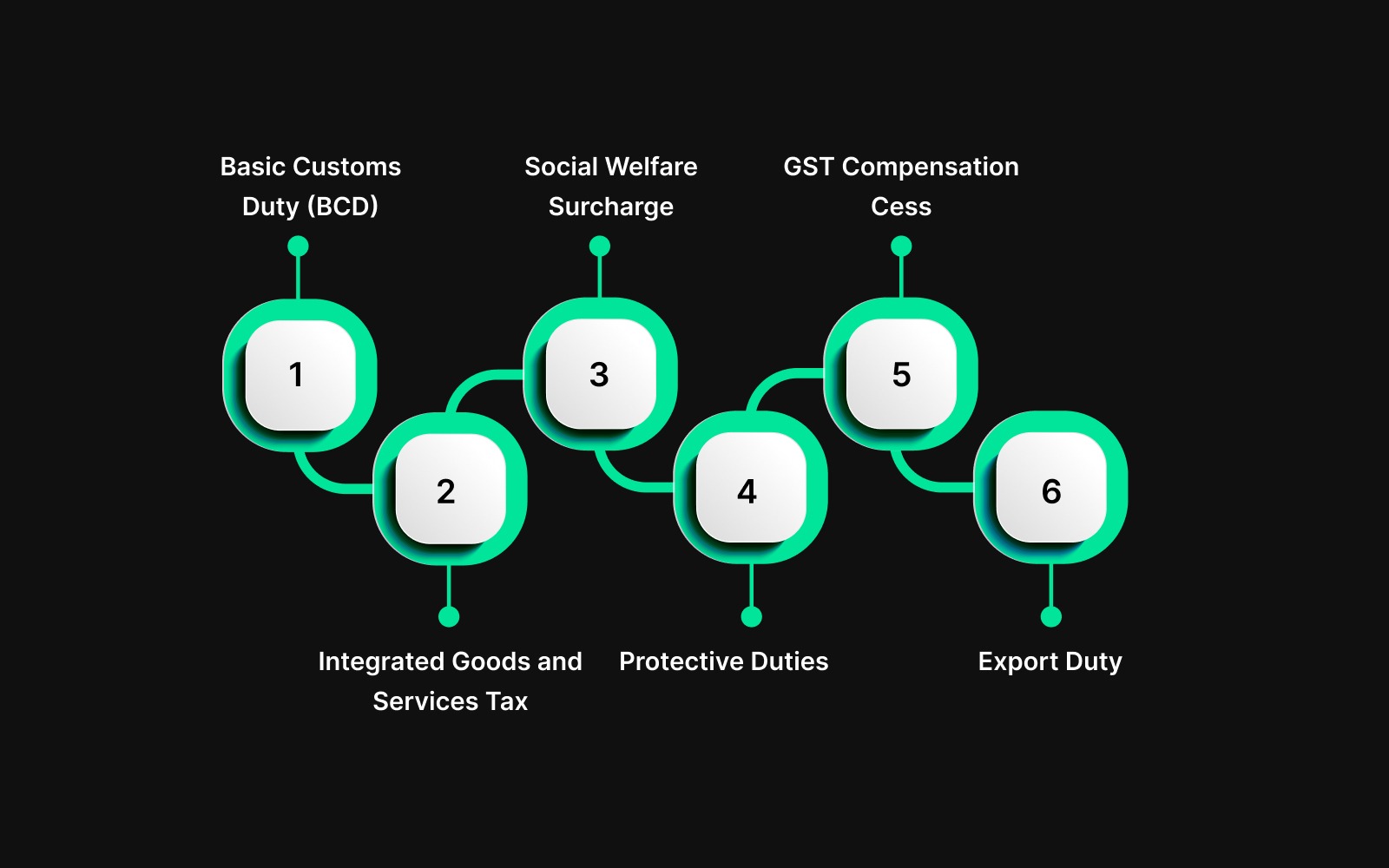

Types of Customs Charges in India

Customs charges in India aren't a single, straightforward tax. They consist of multiple components, each serving a specific purpose. Let's break them down:

Basic Customs Duty (BCD)

Basic Customs Duty is the primary import duty charged on goods entering India. It's levied under the Customs Act, 1962, and the rate varies based on the product's HSN (Harmonised System Nomenclature) code.

According to recent government announcements, India's average customs duty has been reduced to 10.66%, bringing it closer to ASEAN levels. The Union Budget 2025 further rationalised tariff rates to just 8 levels (including zero) to simplify the duty structure.

Most products fall within the 0-20% range, though luxury items and certain goods can attract higher rates. For instance, mobile phones and chargers saw BCD reduced from 20% to 15% in the 2024 budget, whilst non-biodegradable PVC flex banners faced an increase from 10% to 25%.

The Central Government modifies these rates through budget announcements or specific notifications to support domestic manufacturing or regulate imports in line with economic needs.

Also Read: Top HSN Codes Which India Imports and Exports

Integrated Goods and Services Tax (IGST)

IGST on imports replaced several earlier indirect taxes when GST was implemented in 2017. Here's the crucial point: IGST is levied on the assessable value of goods plus the BCD already charged.

The IGST rates are 0%, 5%, 12%, 18%, or 28%, depending on the product category and its HSN code. The good news? If you're a registered GST taxpayer using imported goods for business purposes, you can claim Input Tax Credit (ITC) on the IGST paid.

This means that whilst you pay IGST upfront at customs, you can offset it against your GST liability on domestic sales. However, you cannot claim ITC on the Basic Customs Duty; that's a sunk cost.

Social Welfare Surcharge (SWS)

Social Welfare Surcharge is an additional levy meant to fund government social welfare programmes. It's calculated as 10% of the Basic Customs Duty.

The key thing to remember about SWS: it's charged on the BCD amount, not on the total value of goods. And like BCD, you cannot claim any Input Tax Credit on SWS; it's an additional cost you need to factor into your landed cost calculations.

Protective Duties

India imposes protective duties to safeguard domestic industries from unfair trade practises. These include:

- Anti-Dumping Duty: Levied on goods sold in India below their normal value in the country of origin. For instance, if Chinese steel is being dumped in the Indian market at prices that threaten domestic steel manufacturers, the government may impose an anti-dumping duty.

- Safeguard Duty: Imposed when a sudden surge in imports threatens to harm the domestic industry. This is temporary and meant to give local manufacturers time to adjust.

- Countervailing Duty (CVD): Applied to goods that receive subsidies or tax breaks in their country of origin, ensuring fair competition with Indian products.

These protective duties are product-specific and situation-dependent. You'll need to check the latest notifications from the Central Board of Indirect Taxes and Customs (CBIC) to know if your products attract such duties.

GST Compensation Cess

Certain luxury and demerit goods attract an additional GST Compensation Cess on top of IGST. This includes items like aerated drinks, tobacco products, luxury cars, and coal.

The Cess is calculated on the assessable value plus BCD, similar to IGST. However, unlike IGST, you cannot claim Input Tax Credit on the Compensation Cess.

Export Duty

Here's something many exporters don't realise: whilst India generally promotes exports, certain products are subject to export duties. These are imposed to:

- Conserve domestic resources (like iron ore, bauxite)

- Ensure adequate domestic supply (agricultural products during shortages)

- Achieve specific policy objectives

Export duties are far less common than import duties, but they're not zero. If you're exporting minerals, raw hides, or certain agricultural commodities, check whether export duty applies to your specific product.

Also Read: Standard Operating Procedure for Export Documentation Process

How Are Customs Charges in India Calculated?

Understanding the calculation process is essential for accurate costing. Let's walk through a step-by-step example for importing customs charges in India:

Step 1: Determine the Assessable Value

The assessable value is your starting point. For imports, it's calculated using the CIF (Cost, Insurance, Freight) method:

Assessable Value = FOB Value + Freight + Insurance + Landing Charges

Let's say you're importing machinery worth $50,000 (FOB), with freight of $2,000, insurance of $500, and landing charges of $300.

Assessable Value = $50,000 + $2,000 + $500 + $300 = $52,800

Convert this to Indian Rupees using the exchange rate applicable on the date of the Bill of Entry. At ₹83 per dollar, that's ₹43,82,400.

Step 2: Calculate Basic Customs Duty

Find the BCD rate applicable to your product's HSN code. For machinery, let's assume it's 7.5%.

BCD = Assessable Value × BCD Rate

BCD = ₹43,82,400 × 7.5% = ₹3,28,680

Step 3: Calculate Social Welfare Surcharge

SWS is 10% of the BCD amount.

SWS = BCD × 10%

SWS = ₹3,28,680 × 10% = ₹32,868

Step 4: Calculate IGST

IGST is levied on the assessable value plus BCD. For machinery, assume IGST is 18%.

IGST = (Assessable Value + BCD) × IGST Rate

IGST = (₹43,82,400 + ₹3,28,680) × 18% = ₹47,11,080 × 18% = ₹8,47,994

Step 5: Total Import Duty

Total Customs Charges = BCD + SWS + IGST + Any other applicable duties

Total = ₹3,28,680 + ₹32,868 + ₹8,47,994 = ₹12,09,542

Your total landed cost would be the assessable value plus all these duties: ₹43,82,400 + ₹12,09,542 = ₹55,91,942.

This is the actual cost you need to factor into your pricing, procurement decisions, and cash flow planning.

Important Calculation Notes

The order matters: BCD is calculated first on the assessable value, then IGST is calculated on the assessable value plus BCD. You can't reverse this sequence.

Always verify the HSN code classification carefully. A wrong HSN code can lead to incorrect duty rates, penalties, and delayed clearances.

Use the official ICEGATE duty calculator or consult with a licenced customs broker to ensure accuracy, especially for complex products or first-time imports.

Must Read: What is the HS Code in Imports and Exports? A Beginner's Guide

When Do Customs Charges Apply?

Understanding when customs charges in India are triggered helps you plan better and avoid surprises.

On Imports

Customs charges apply to virtually all goods imported into India, with a few exceptions:

- Goods imported under the duty-free allowance for personal use (limited value and quantity)

- Items covered by government exemption notifications

- Goods imported into Special Economic Zones (SEZs) or Export-Oriented Units (EOUs) under specific schemes

- Products from countries with Free Trade Agreements (FTAs) where preferential duty rates apply

Even if your goods qualify for exemptions, you still need to file proper documentation and follow customs clearance procedures.

On Exports

Export duties in India are the exception, not the rule. They typically apply to:

- Minerals and ores (iron ore fines, lumps, pellets; bauxite)

- Raw hides and skins (to encourage domestic leather processing)

- Certain agricultural products during shortage periods

- Onions during domestic supply crunches (temporary measures)

The government regularly updates the list of goods subject to export duty through notifications. Always check the latest export policy before finalising your shipment.

For most manufactured exports, you won't pay export duties. In fact, you might be eligible for duty drawback, refunds on import duties paid on raw materials used in manufacturing export goods.

On Re-Imports and Re-Exports

If you export goods and they're returned to India (for repairs, warranty claims, or rejection), customs charges may apply depending on the reason for return and the time elapsed.

Similarly, if you import goods temporarily for exhibitions, testing, or processing, and re-export them, different customs regimes apply that can reduce or eliminate duties.

Time-Sensitive Scenarios

Customs charges are payable at the time of customs clearance, before goods are released. Delays in payment can result in:

- Demurrage charges from shipping lines or airlines

- Storage costs at customs warehouses

- Interest on delayed duty payments

- Penalties for non-compliance

Also Read: Best practises for Customs Documentation and Labelling for International Shipments

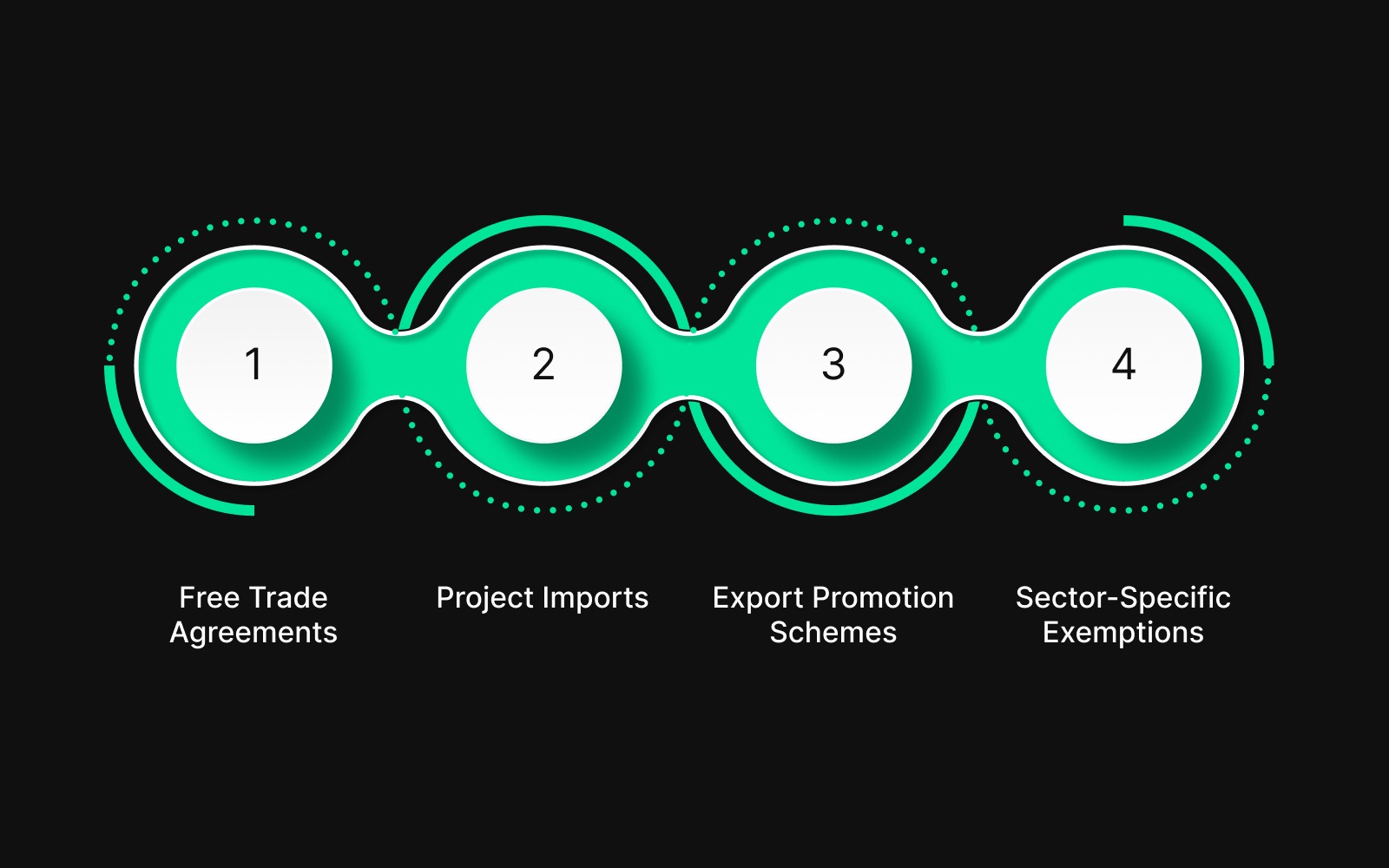

Exemptions and Concessions on Customs Charges in India

Not all imports and exports attract the full rate of customs charges. Here are key exemptions you should know about:

Free Trade Agreements (FTAs)

India has FTAs with several countries and trading blocs, including ASEAN nations, Japan, South Korea, and the UAE. Under these agreements, products that meet the Rules of Origin (RoO) criteria can enjoy reduced or zero BCD.

For example, if you're importing textiles from Japan under the India-Japan CEPA, you might pay 0% BCD instead of the standard rate, provided the goods meet origin requirements, and you have the necessary certificate of origin.

Project Imports

Capital goods and equipment imported for specific projects (power plants, refineries, infrastructure) can qualify for concessional duty rates under project import regulations.

Export Promotion Schemes

Exporters can benefit from schemes like:

- Duty Drawback: Get refunds on import duties paid on raw materials used in export production

- Advance Authorisation: Import duty-free inputs for manufacturing export products

- EPCG Scheme: Import capital goods at concessional or zero duty for export production

Sector-Specific Exemptions

The government periodically announces exemptions for specific sectors to promote domestic manufacturing. Recent budget announcements have included exemptions for:

- Lithium-ion battery manufacturing equipment

- Shipbuilding materials

- Critical minerals for green energy

- Life-saving medicines and medical equipment

- Agricultural machinery and inputs

Always check the latest notifications from CBIC and the Directorate General of Foreign Trade (DGFT) to see if your products qualify for any exemptions.

How Pazago Supports Exporters at the Logistics and Customs Execution Layer

Understanding customs charges in India is only half the battle. The real challenge begins when those charges intersect with shipment timelines, container availability, documentation handovers, and payment coordination. Even accurate duty calculations can fall apart if logistics execution is misaligned.

Pazago supports exporters at this execution layer, where customs, freight movement, and shipment coordination meet.

Coordinated Logistics That Prevent Customs Delays

Pazago works with exporters to ensure that shipment planning, container booking, and document readiness move in sync. By coordinating logistics milestones with customs timelines, exporters reduce last-minute scrambling and avoid avoidable penalties.

Clear Visibility Across Long Export Cycles

Pazago provides exporters with consistent shipment visibility through daily status updates covering container movement, vessel ETD and ETA changes, and clearance progress. This visibility helps exporters anticipate when customs charges will apply and prepare documentation and payments ahead of time.

Single Point of Coordination Across Stakeholders

Pazago acts as a central coordination layer, helping exporters manage logistics conversations at the order level. Shipment updates, customs-related clarifications, and documentation follow-ups stay linked to the shipment itself, reducing confusion when multiple orders are active.

Supporting Exporters of All Sizes

Pazago supports exporters across volumes and experience levels, ensuring that logistics coordination, shipment visibility, and execution discipline remain consistent. Whether it is a single container or recurring shipments, exporters receive the same structured support.

Conclusion

Customs charges in India are a core part of your export cost structure. From Basic Customs Duty and IGST to Social Welfare Surcharge and protective duties, each component directly impacts pricing and compliance.

Managing these charges comes down to three essentials: accurate HSN classification, staying up to date on notifications and exemptions, and maintaining clean documentation. Even a small error can lead to higher duties or missed benefits under FTAs and export schemes.

If customs charges, shipment timelines, and logistics coordination are starting to feel disconnected, it’s time to bring them onto one operational track. Pazago works with exporters to align freight movement, documentation readiness, and shipment visibility so customs processes support your exports instead of slowing them down.

Speak with the Pazago team to understand how your export logistics can run with fewer delays and clearer control. Book a consultation today.

Frequently Asked Questions

1. Can I get a refund on customs charges paid?

For imports used in manufacturing export goods, you can claim duty drawback refunds on customs charges paid. For IGST, you can claim Input Tax Credit if you're a registered GST taxpayer. However, BCD and SWS are generally not refundable, except under specific export promotion schemes such as Advance Authorisation.

2. How do I find the correct HSN code for my product?

You can search for HSN codes on the CBIC website or the ICEGATE portal. Enter your product description, and the system will suggest applicable codes. For complex products, it's advisable to consult a licenced customs broker or seek an Advance Ruling from customs authorities to avoid classification disputes.

3. What happens if I don't pay customs charges on time?

Delays in payment of customs charges result in interest charges, carrier demurrage fees, storage costs at customs warehouses, and potential penalties. In extreme cases, goods can be auctioned by customs if duties remain unpaid for extended periods. Always ensure funds are available before your shipment arrives.

4. Are customs charges the same for all ports in India?

The duty rates are uniform across all Indian ports, as they're set by the Central Government. However, port-specific charges like handling fees, storage costs, and documentation charges may vary. The method of duty calculation remains the same regardless of the port of entry.

5. Do Free Trade Agreements eliminate all customs charges?

FTAs typically eliminate or reduce Basic Customs Duty on qualifying goods that meet the Rules of Origin criteria. However, you'll still need to pay IGST, SWS, and other applicable charges. The benefit primarily lies in the BCD component, which can be substantial but doesn't eliminate all customs-related costs.