.png)

What Is High Sea Sales? Process, GST Rules & Customs Impacts

Optimize your business: use unlimited savings with Pazago fulfilled now!

Get Started ->If you are an exporter, chances are you have come across high sea sales. It is a legitimate and widely used trade structure where the buyer changes after the goods are dispatched from the origin port but before the goods are entered for import.

In this narrow window, ownership transfers while the cargo is in transit. That single action determines who becomes the importer, whose invoice customs accepts for valuation, and how taxes are applied at the time of clearance. When the sequence is handled correctly, high sea sales work as intended. When it is not, the same shipment can face reassessment, duty disputes, or clearance delays.

These issues rarely appear when the sale is agreed. They surface when the Bill of Entry is filed, and customs examines the ownership chain and document sequence. This guide explains how high sea sales operate in practice and where exporters most often lose control during execution.

Key Takeaways

- High sea sales involve a change of ownership while goods are in transit, before the shipment is entered for import, and are a legally accepted trade structure.

- Ownership transfer timing determines whether customs accepts or ignores a high sea sale. Late execution invalidates the resale, even if the commercial agreement exists.

- The final buyer in the high sea sale chain is treated as the importer and bears customs duty and IGST liability at the time of clearance.

- GST is not charged on the high sea sale itself, but IGST is collected at import, which often creates confusion around tax exposure and ITC.

- High sea sales require tight operational control during transit, as errors surface only when the Bill of Entry is filed and clearance begins.

What Is High Sea Sales in International Trade

High Sea Sales (HSS) refer to a unique type of sale that transpires when goods are in transit between the exporting and importing countries. This method allows trading of goods without physical handling by the seller or original buyer.

During a high sea sale, the current owner endorses or assigns the transport documents, such as the bill of lading or airway bill, effectively transferring goods' ownership while they are still at sea. HSS in India falls under the 'in the course of import' category per Section 5(2) of the Central Sales Tax Act, 1956.

For example, goods are shipped from China to India under a bill of lading issued to an Indian buyer. While the vessel is still in transit and before the Bill of Entry is filed, the buyer sells the goods to another buyer, such as a company based in Chennai, by executing a High Sea Sale Agreement and endorsing the bill of lading. The Chennai buyer then becomes the importer for customs purposes, and duty and taxes are assessed based on the high sea sale invoice.

Difference Between Regular Imports And High Sea Sales

Regular imports and high sea sales follow the same physical shipment, but the commercial ownership and customs treatment differ materially. Below is a side-by-side comparison of regular imports and high sea sales, highlighting differences in ownership, documentation, and customs treatment.

Legality Of High Sea Sales Under Customs And GST

High sea sales are legally recognized under both customs and GST law in India, but their treatment depends entirely on when ownership transfers and who the final buyer is.

GST Treatment Of High Sea Sales

Under Section 7(2) of the IGST Act, goods imported into India are treated as an inter-state supply until they cross the customs frontiers of India. In practice, this means the GST outcome depends on the final buyer's location.

When the final buyer is in India:

- High sea sales executed before import filing are not taxed at the time of sale.

- IGST is levied only once, at the time of import, when the Bill of Entry is filed.

- The last buyer in the high sea sale chain pays IGST during customs clearance.

- Any value added during high sea sales is included in the taxable value for IGST.

GST authorities have clarified that even if there are multiple high sea sales, IGST is collected only at import, not on each resale.

When the final buyer is outside India:

- If goods are sold from one non-taxable territory to another non-taxable territory without entering India, the transaction is outside the scope of GST.

- This treatment comes from amendments to Schedule III of the GST law.

- No GST applies to such merchant trade transactions, provided the goods do not enter India.

Customs Duty And Valuation In High Sea Sales

From a customs perspective, high sea sales do not change the physical import of goods. Customs focuses on who owns the goods at the time of import.

- The last high sea buyer is treated as the importer.

- That buyer files the Bill of Entry and pays customs duty and IGST.

- Customs duty is assessed on the transaction value of the last sale, not the original supplier invoice.

As a general practice, customs considers high sea sale charges at around two percent of the CIF value. However, if the actual high sea sale price is higher, customs uses the actual transaction value for assessment. IGST is then calculated on this value plus applicable customs duties and cess.

High sea sales are legal, but customs validates them only at the time of import. If the ownership transfer, invoice trail, or valuation linkage between the first and last sale is unclear, customs can reject the declared value or reopen the assessment. This is why documentation sequence and timing matter more than commercial intent.

Documents Required For High Sea Sales

High sea sales do not require separate registration with customs, but they are verified in detail at the time of Bill of Entry assessment and out-of-charge. Customs evaluates the transaction based on document continuity, timing, and ownership transfer.

The following documents are mandatory for high sea sales clearance, as prescribed under CBEC Circular No. 14/2014 and subsequent public notices.

Mandatory High Sea Sale Documents

- High Sea Sale Agreement: Executed between the seller and the high sea buyer. The agreement must be signed by both parties and duly notarized. If notarization is not available, bank attestation by an authorized signatory is required. The agreement date must be on or before the IGM filing date.

- Bill of Lading (Endorsed): A non-negotiable copy of the bill of lading, duly endorsed in favor of the high sea buyer. If the original is unavailable, a copy authenticated by the shipping line, steamer agent, or customs broker is accepted.

- Commercial Invoice (Original Supplier): Issued by the overseas supplier to the original buyer, forming the base of the ownership chain.

- High Sea Sale Invoice: Issued by the high sea seller to the high sea buyer, reflecting the resale value and any value addition.

- IEC Copies Of Buyer And Seller: Import Export Code documents of both parties involved in the high sea sale transaction.

- Authority Letter For Customs Broker: Authorization from the high sea buyer if a customs broker is appointed for filing the Bill of Entry.

How Customs Verifies These Documents

Customs officers verify high sea sales during assessment and before granting out-of-charge, not at a separate registration desk. The checks typically include:

- Validity and timing of the High Sea Sale Agreement.

- Endorsement and ownership continuity on the bill of lading.

- Invoice linkage between the supplier invoice and the high sea sale invoice.

- Correct declaration of high sea sale details in the Bill of Entry.

- Disclosure of high sea sale commission, if any.

Where multiple high sea sales exist, documents for each resale must be submitted together.

Even when all documents are present, customs may reject the transaction if the dates, endorsements, or invoice values do not align. This is why document control during transit is critical.

Also read: Important Documents Required for Export

What Is The Procedure For High Sea Sales?

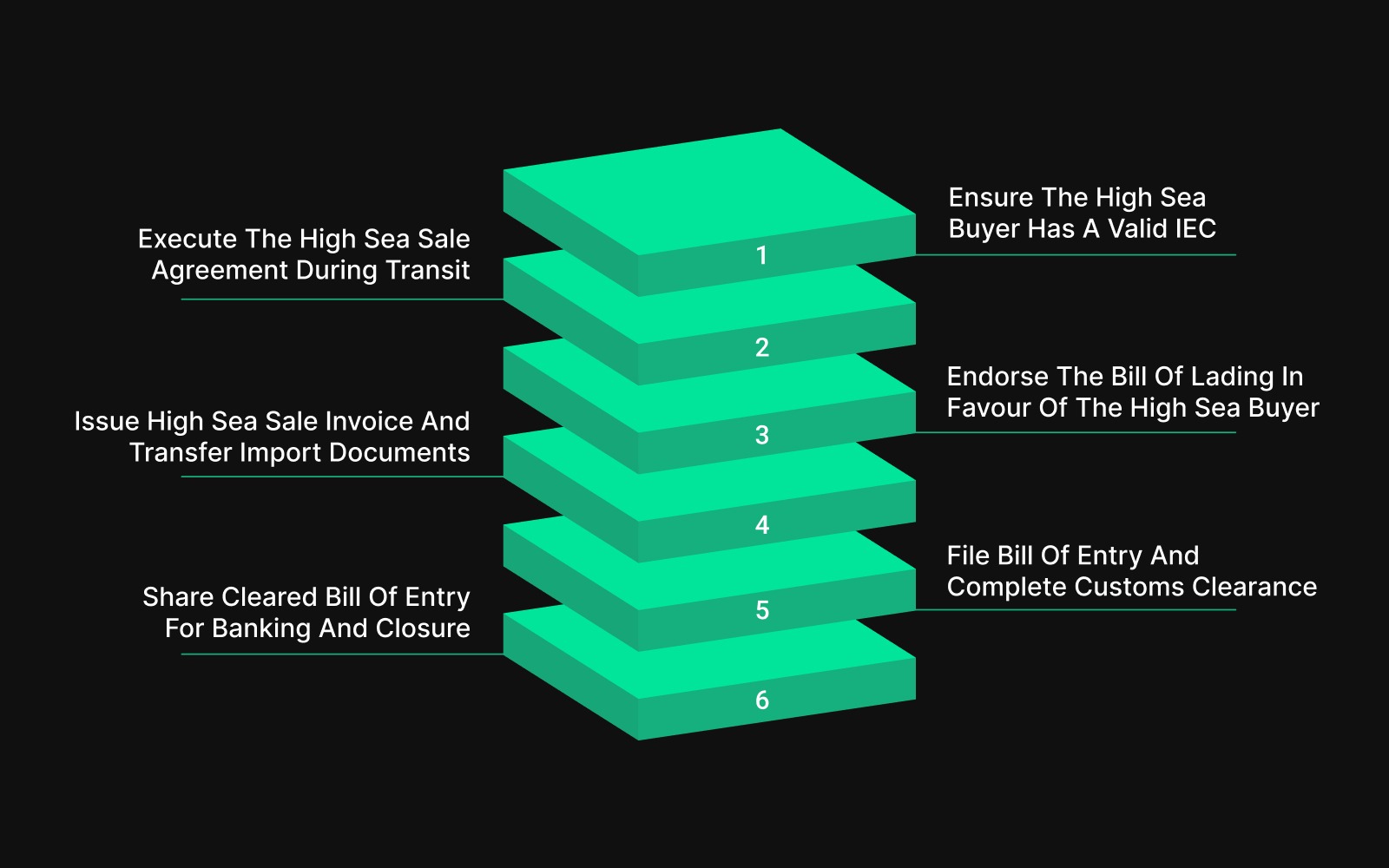

High sea sales follow a fixed operational sequence. The steps must occur in order and within the correct time window, or customs will reject the transaction during import assessment.

Step 1: Ensure The High Sea Buyer Has A Valid IEC

The high sea buyer must hold a valid Import Export Code (IEC) issued by DGFT. Without an IEC, the buyer cannot act as the importer or file the Bill of Entry. This is a basic eligibility requirement before any high sea sale is executed.

Step 2: Execute The High Sea Sale Agreement During Transit

After the goods are dispatched from the exporter’s country and while they are still in transit, the original buyer enters into a High Sea Sale Agreement with the new buyer.

The agreement must be executed on stamp paper and duly notarized. Its date must fall before the import filing and within the transit period.

Step 3: Endorse The Bill Of Lading In Favour Of The High Sea Buyer

The original buyer endorses the bill of lading or airway bill in favour of the high sea buyer. This endorsement legally transfers title of the goods during transit and establishes the high sea buyer as the future importer.

Step 4: Issue High Sea Sale Invoice And Transfer Import Documents

The high sea seller issues a high sea sale invoice to the buyer, typically in INR. Along with this invoice, the seller provides the full document set required for import clearance, including:

- Original or endorsed bill of lading

- Supplier commercial invoice

- Packing list

- Certificate of origin

- Insurance documents

These documents form the ownership and valuation chain that customs later verifies.

Step 5: File Bill Of Entry And Complete Customs Clearance

The high sea buyer files the Bill of Entry for home consumption, declaring themselves as the importer and disclosing high sea sale details. Customs duty and IGST are paid by the high sea buyer based on the declared value.

In cases where the high sea seller does not want to disclose the original supplier price to the buyer, the seller may retain control of customs clearance and file documents on behalf of the buyer through an authorized customs broker.

Step 6: Share Cleared Bill Of Entry For Banking And Closure

After customs clearance, the high sea buyer shares a copy of the cleared Bill of Entry with the high sea seller. The seller submits this, along with other high sea sale documents, to the bank for transaction closure and record purposes.

Key Case Laws On High Sea Sales

There are a few important case laws that provide clarity on how high sea sales are treated under customs and GST. These rulings explain when GST applies, who pays IGST at import, and which value customs uses for assessment. The cases below show how authorities have applied these rules in real high sea sale transactions.

1. BASF India Ltd. (Authority for Advance Ruling – Maharashtra)

BASF India purchased goods from overseas suppliers based on confirmed orders from its customers. Before the goods crossed the customs frontier of India, BASF sold them to those customers under high sea sales. The question was whether IGST applied to these sales and whether the input tax credit needed to be reversed.

The ruling: The Authority held that IGST does not apply to high sea sales executed before the goods cross the customs frontier. However, IGST is payable at the time of import by the final buyer who clears the goods. Since the high sea sale was treated as an exempt supply, BASF was required to reverse the input tax credit related to that transaction.

2. Commissioner of Customs (Imports) v. Shree Krishna Enterprises (2019)

The dispute concerned whether customs duty should be calculated based on the original supplier price or the high sea sale price, and whether GST applied to the high sea sale.

The ruling: The Supreme Court held that customs duty must be assessed on the value of goods at the time of import, payable by the buyer who clears the goods. High sea sales were recognized as sales in the course of export, and GST was held to be inapplicable on the resale itself.

3. South India Trading Co. v. Commissioner of Customs (2016)

The case was whether goods imported under high sea sales were liable to customs duty and GST based on resale value.

The ruling: The Tribunal confirmed that customs duty is payable based on the declared transaction value at import. GST does not apply to the high sea sale, while IGST is levied at import and can be claimed as input tax credit by the importer, subject to compliance.

Across rulings, authorities have taken a consistent position. High sea sales are legally valid when ownership transfers during transit. GST is not levied on the resale itself, but customs duty and IGST are collected at the time of import from the final buyer.

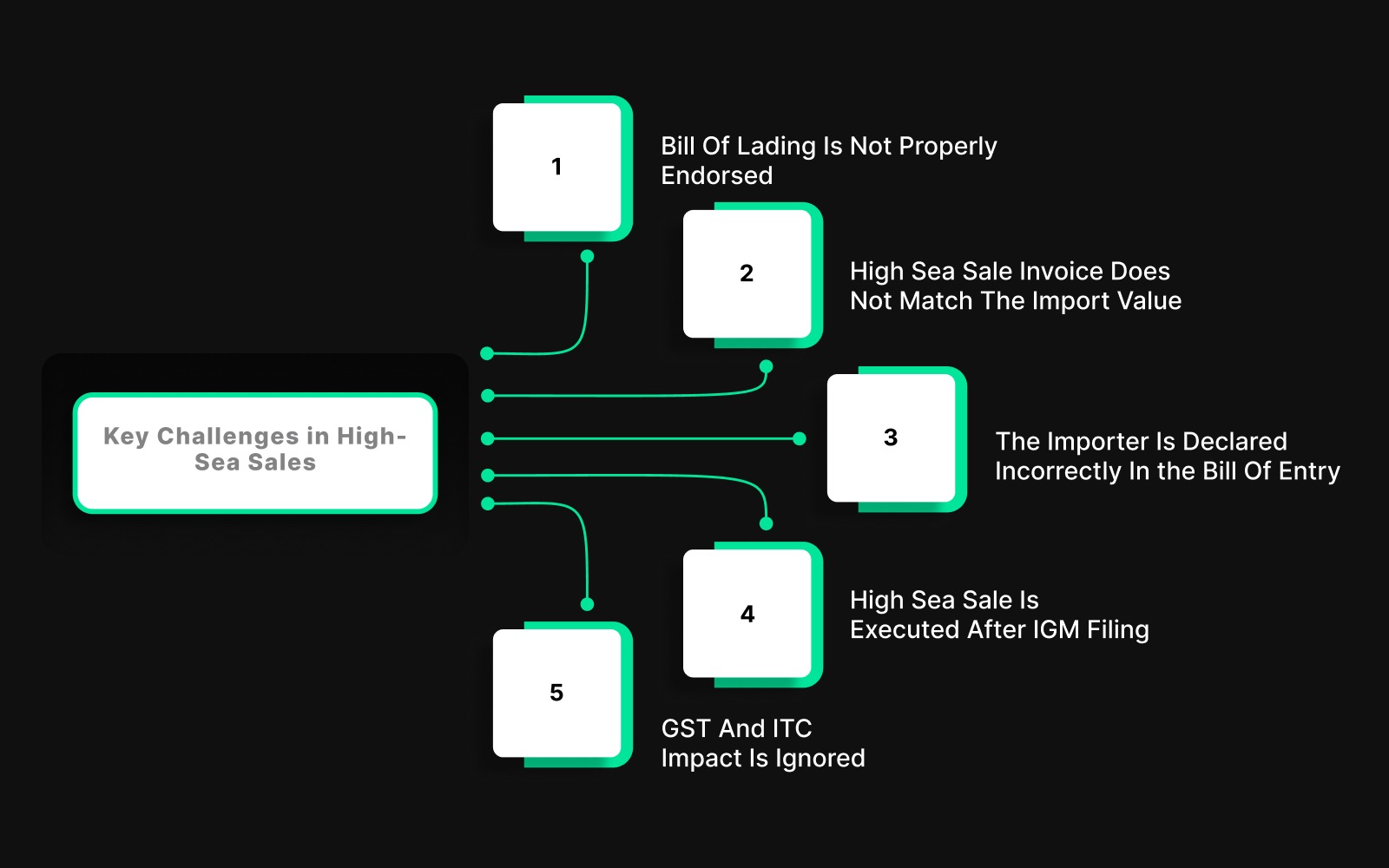

Challenges In High Sea Sales And How To Solve Them

High sea sales fail less because of intent and more because of execution gaps during transit. Below are the most common problem areas exporters and traders face, explained with practical fixes.

1. Bill Of Lading Is Not Properly Endorsed

The agreement exists, but the bill of lading still shows the original buyer or is endorsed incorrectly. Customs relies on the bill of lading to establish ownership. Without a clear endorsement, the sale is ignored.

How to avoid it: Ensure the bill of lading is endorsed in favor of the high sea buyer and matches the agreement date and invoice sequence.

2. High Sea Sale Invoice Does Not Match The Import Value

The declared import value does not reflect the high sea sale price or value added during resale. Customs assesses duty and IGST based on the last transaction value. Mismatch triggers reassessment.

How to avoid it: Declare the complete price chain and ensure the high sea sale invoice aligns with the Bill of Entry value.

3. The Importer Is Declared Incorrectly In the Bill Of Entry

The original buyer files the Bill of Entry even though ownership has transferred. Customs assigns duty and tax liability to the importer of record. Wrong importer leads to disputes.

How to avoid it: The high sea buyer must file the Bill of Entry and be declared as the importer.

4. High Sea Sale Is Executed After IGM Filing

The agreement date or notarization date falls after the IGM filing. Customs treats this as a post-import sale, which has no relevance for valuation or tax.

How to avoid it: Execute and notarize the agreement before IGM filing, with dates clearly traceable.

5. GST And ITC Impact Is Ignored

Exporters assume no GST impact and later face ITC reversals or audit queries. High sea sales shift tax timing, not tax liability.

How to avoid it: Account for IGST at import and assess ITC implications upfront.

High sea sales are not complex. They are time-bound. When ownership transfer, document sequence, and import filing line up, customs accepts the transaction. When they don’t, the sale is ignored.

How Pazago Supports High Sea Sales Execution During Transit

High sea sales succeed or fail during transit, not at the time of the commercial agreement. Ownership transfer, document endorsement, and timing must align precisely before import filing triggers customs scrutiny.

Where exporters lose control is in execution. Freight availability, container readiness, loading coordination, and shipment visibility often run in parallel while ownership is changing. When these activities are not aligned, agreements exist on paper but fail during clearance.

Pazago supports exporters handling high sea sales by strengthening logistics execution at this critical stage:

- Competitive freight rates across key trade lanes, helping exporters plan shipments without last-minute booking disruptions

- Assured container booking and coordinated factory, CFS, or port loading to align movement with ownership-transfer timelines

- Daily Status Reports (DSRs) covering container movement, ETD/ETA changes, transshipment updates, and BL status

- Hands-on pre-shipment and post-shipment support to resolve coordination issues while the cargo is still in transit

- Equal operational support for exporters of all sizes, including one-off and recurring high sea sale transactions

By tightening control over shipment execution during transit, Pazago helps exporters reduce clearance risk caused by timing gaps and coordination failures.

Conclusion

High sea sales are legally accepted, but they leave little margin for execution errors. Ownership must transfer at the correct time, documents must follow a strict sequence, and shipment milestones must remain aligned until import filing.

While the legal structure is well defined, most high sea sale failures originate from execution gaps during transit. Delays in freight confirmation, loading coordination, or shipment visibility often push ownership actions outside the valid window.

Pazago supports exporters managing high sea sales by focusing on logistics execution reliability. With stable freight rates, assured container bookings, coordinated loading, daily shipment status reporting, and hands-on operational support, Pazago helps exporters maintain control throughout cargo movement.

FAQs On High Sea Sales

1. When does a high sea sale become invalid?

A high sea sale becomes invalid when ownership transfer happens after the import process has effectively started. If the High Sea Sale Agreement or bill of lading endorsement is executed after the Bill of Entry is filed or after IGM timelines are breached, customs treats the transaction as a regular import.

2. Can there be multiple high sea sales for one shipment?

Yes. Multiple high sea sales are permitted as long as each resale happens during transit and before import filing. Customs requires a complete and continuous document chain covering every resale, with clear dates, invoices, and bill of lading endorsements.

3. Is GST charged on high sea sales?

GST is not charged on the high sea sale transaction itself. IGST is collected only at the time of import from the final buyer who clears the goods through customs. The tax liability is deferred, not removed.

4. Who pays Customs Duty and IGST in high sea sales?

The last buyer in the high sea sale chain pays customs duty and IGST at the time of import. That buyer is treated as the importer for customs purposes and files the Bill of Entry.

5. Can high sea sales be done if the final buyer is outside India?

Yes. If goods are sold from one non-taxable territory to another non-taxable territory without entering India, the transaction falls outside the scope of GST. This is treated as merchant trade, provided the goods never enter the taxable territory of India.